Just as the narrative around the great metals supercycle was reaching a peak of enthusiasm, the market suddenly reversed with a historic crash. Markets have a particular ability to surprise and leave many market participants in a state of shock. As Warren Buffett famously said, only when the tide goes out do you discover who has been swimming naked: while the trend is favourable, everything appears to work; when difficulties emerge and volatility returns, many participants exit the market, often at the worst possible moment.

Before going into detail, we would like to remind you that we have published our first exclusive report, dedicated to NGEx Minerals. It is an independent, technical and in-depth analysis of one of the most successful exploration companies of the current cycle, in which we assess risks, opportunities and valuation scenarios beyond the headlines. The report is available both to our community, with a special launch offer currently in place, and through individual purchase.

Take advantage of the launch offer

Without further delay, we will attempt to break down the most relevant developments in the macro environment and metals markets during what has been a heart-stopping month. While it would be tempting to focus only on the most recent events, we believe there is value in taking a chronological approach and highlighting developments that may already feel forgotten, but which have had, and may continue to have, a meaningful impact.

Macro environment

Rising geopolitical tensions and growing doubts about U.S. credibility

January began with a renewed increase in geopolitical tension, initially around Venezuela (a focus we already covered in the previous newsletter), and also involving Iran, episodes that have since faded into the background. The next flashpoint emerged around Greenland. Comments from Donald Trump briefly reignited tariff tensions with Europe and brought geopolitics back to the centre of the market’s attention.

The territory’s supposed strategic appeal, particularly due to its natural resources and rare earth elements, returned to the debate, although more detailed analysis suggests its economic relevance is being widely overstated. The episode proved short-lived: the well-known TACO trade (Trump Always Chickens Out) quickly took hold. Trump softened his stance, tensions eased, and the issue once again became political noise… until the next headline.

Despite their fleeting nature, we do not believe such episodes are harmless. The accumulation of contradictory messages and abrupt shifts in rhetoric undermines U.S. institutional credibility. This effect was amplified by the investigation launched against Jerome Powell, which the market interpreted as another form of political pressure on the Fed Chair (and an attack on its independence), whom Trump has repeatedly criticised for not pursuing a more aggressive monetary easing policy.

Subsequently, further comments from the President expressing satisfaction with a weaker dollar added renewed pressure on the U.S. currency. Taken together, these developments heightened institutional concern, weakened the dollar and reinforced demand for precious metals as monetary safe havens.

Performance of U.S. equities (green) and the dollar (red) in 2026

The accumulation of headlines had a clear effect: perceptions of political volatility increased and the narrative of “Sell America” resurfaced in the market. In this context, statements from large European pension funds stood out, as they began to question their high concentration in U.S. assets given growing unpredictability and institutional uncertainty.

The month, however, ended with a partial reversal following the nomination of Kevin Warsh as a potential future Chair of the Federal Reserve. The market initially interpreted this move as hawkish, restoring some institutional credibility and allowing for a moderate recovery in the dollar. This, in turn, acted as a catalyst for the crash in precious metals on Friday the 30th (more on this shortly). That said, views on Warsh remain mixed, and his credibility as a genuine advocate of tight monetary policy has yet to be proven (particularly given Trump’s preferences and political interference), leaving the outlook highly uncertain.

At the same time, Japan returned to the spotlight. The debate around monetary normalisation and the sharp rise in interest rates, together with their implications for the yen and global capital flows, added another layer of uncertainty. This introduced second-order risks for global financial markets at a time of heightened sensitivity to changes in monetary policy.

Metals markets

Between the growing strategic importance of metals (greater government intervention), risks of euphoria, and the Great Crash of January 30

Gold and silver

What unfolded during the month warrants a more extensive discussion of precious metals, with a particular focus on gold and silver, although the moves also reverberated across platinum, palladium and other metals.

% performance of gold (ochre) and silver (grey) in 2026

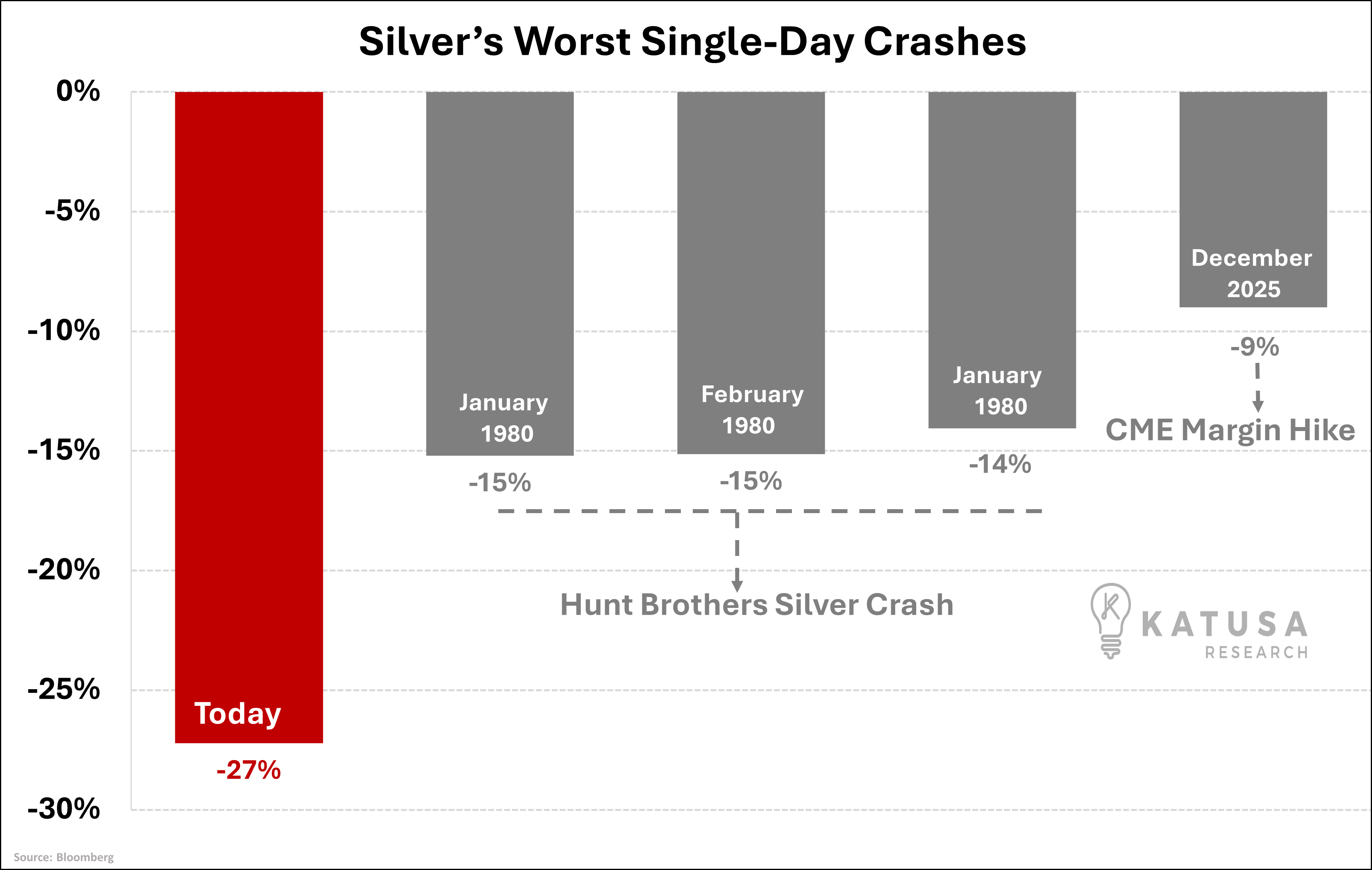

The chart above will likely go down in market history books. Let us break it down step by step. In the initial phase, monetary metals were once again the main beneficiaries of the macro environment described earlier. The early part of the move was relatively orderly, driven by growing concerns over the credibility of the United States as the anchor of the global fiat monetary system, with the dollar at its core, among other factors.

The well-known and influential investor Ray Dalio commented on this dynamic as follows: “It’s the beginning of the end of the monetary system as we know it, the fiat monetary currencies, not only the dollar. This is why gold is being chosen by the central banks, they want a currency (gold has always been the main currency, it’s the only non-fiat currency, not the currency that can be printed). That’s the nature of the shift of the monetary system.”

By late in the month, the strength of the move was extraordinary. Gold had risen by more than 20% year-to-date (in less than a month), while silver entered an explosive phase, characteristic of its historical behaviour, climbing by more than 60% to levels close to $120. Silver moved to the centre of media attention and investment forums alike, with a clear increase in FOMO among retail investors. Sentiment became excessively positive and volatility (at that stage only to the upside) was extreme, with a clearly parabolic advance that was unlikely to be sustainable.

Social media was flooded with rumours and various forms of misinformation, alongside heated debates around manipulation narratives, immediate physical shortages and price premiums between Western markets and Shanghai.

In our previous newsletter, we warned about the need for prudence before the move reached its most extreme phase. That call was undoubtedly early and would have meant missing part of the subsequent rally (from $80 to $120), but it was precisely that extension of the move that ultimately stretched the market to an unsustainable point, laying the groundwork for a violent correction.

That correction arrived abruptly on Friday the 30th. While a complete and precise explanation is difficult (and not our main focus, which remains on medium- and long-term dynamics), our interpretation, supported by different sources, is that the crash began to take shape following the tightening of trading conditions in Chinese markets, which directly affected highly leveraged positions and curtailed the buying flow from China that had supported the final leg of the rally. In an already fragile environment, the nomination of Kevin Warsh as a potential future Chair of the Federal Reserve helped drive a rebound in the dollar and acted as the primary catalyst.

With prices clearly overbought, sentiment “hot” and leverage elevated, the adjustment turned into a technical episode of historic magnitude, involving forced liquidations (margin calls) and a rapid unwinding of positions in futures, ETFs and options, which dramatically amplified the decline. As often happens in such episodes, to put it graphically, the exit door became far too narrow for a market that was excessively positioned and leveraged in a single direction.

Following these moves, it appears evident that the gold and silver markets are going through a phase in which, at least in the short term, technical and psychological factors weigh as heavily as fundamentals, making risk management particularly critical. In this context, we believe it is worth sharing the following quote from Howard Marks:

The structural strength and fundamental drivers underpinning the positive trend in precious metals remain intact. As Warren Pies has repeatedly pointed out, in bull markets gold tends to rise much more, and for much longer, than most investors anticipate.

At the time of writing, gold and silver have experienced a strong rebound from their lows, only to retrace part of that move, with gold trading below $4,900 and silver below $80. Regardless of short-term price action, where volatility remains very high, this correction has likely cleansed the market of a significant portion of prior excesses, something that is constructive for the medium-term trend.

Are you a company or an institutional investor in need of an expert, multidisciplinary, and independent evaluation of mining projects? We may be able to help.

Copper

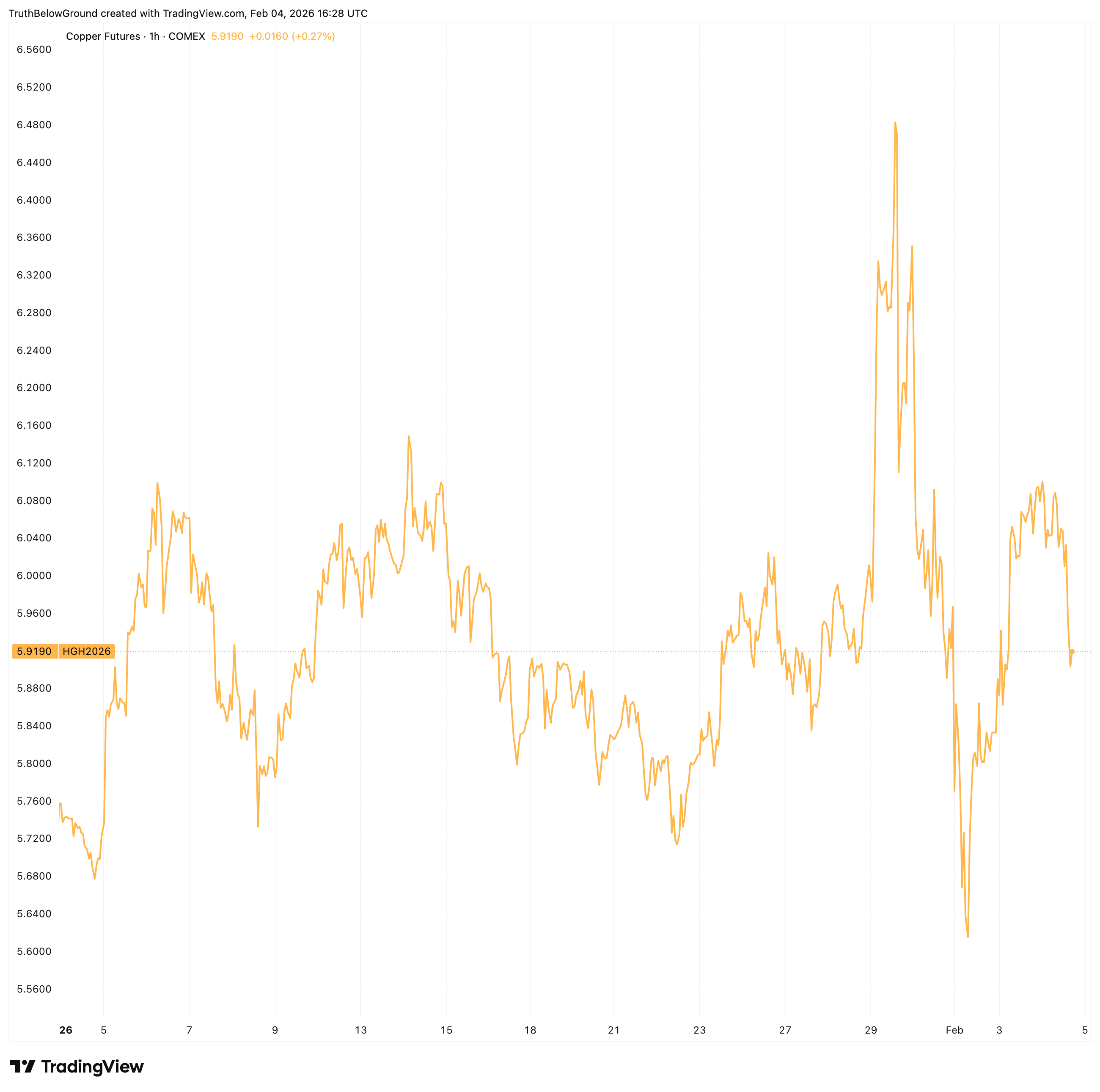

Copper also experienced a volatile month, influenced by the broader dynamics discussed above, but with metal-specific factors playing a key role in price action.

The start of the year was positive, but as we already warned in the previous newsletter, the risk of corrections had increased. Elevated prices were beginning to weigh on real demand, while inventories were showing signs of accumulation, leaving the market vulnerable to short-term adjustments.

Copper performance in 2026

These corrections initially unfolded in a measured way, against the backdrop of the moderately negative market environment observed in mid-January and discussed in the macro section. That weakness proved short-lived, and the upward trend quickly resumed, reaching a climax on January 29, a session marked by an unusually strong price increase, likely amplified by financial and technical dynamics (see Robert Friedland’s comments here). On that same day, just ahead of the following session’s decline, Ole Hansen, Head of Commodity Strategy at Saxo, noted that despite a supportive macro backdrop, micro indicators were not confirming the rally.

Source: Source.

The sell-off the following day can be interpreted as a reversal of that excessive move, exacerbated by the crash in precious metals, which acted as a contagion factor, triggering broader risk reduction across the entire commodities complex.

Over the medium term, the backdrop remains constructive. Both the United States, through Project Vault (discussed below), and China are advancing plans to strengthen strategic copper reserves. At the same time, structural tailwinds persist, driven by rising AI-related capex on the demand side, and supply rigidity and a lack of new projects on the supply side.

In conclusion, the structural copper thesis remains intact, but January made it clear, much like in precious metals, that sharp, vertical moves not supported by short-term fundamentals tend to reverse quickly, particularly in a highly volatile metals environment where correlations can spike regardless of each metal’s specific fundamentals.

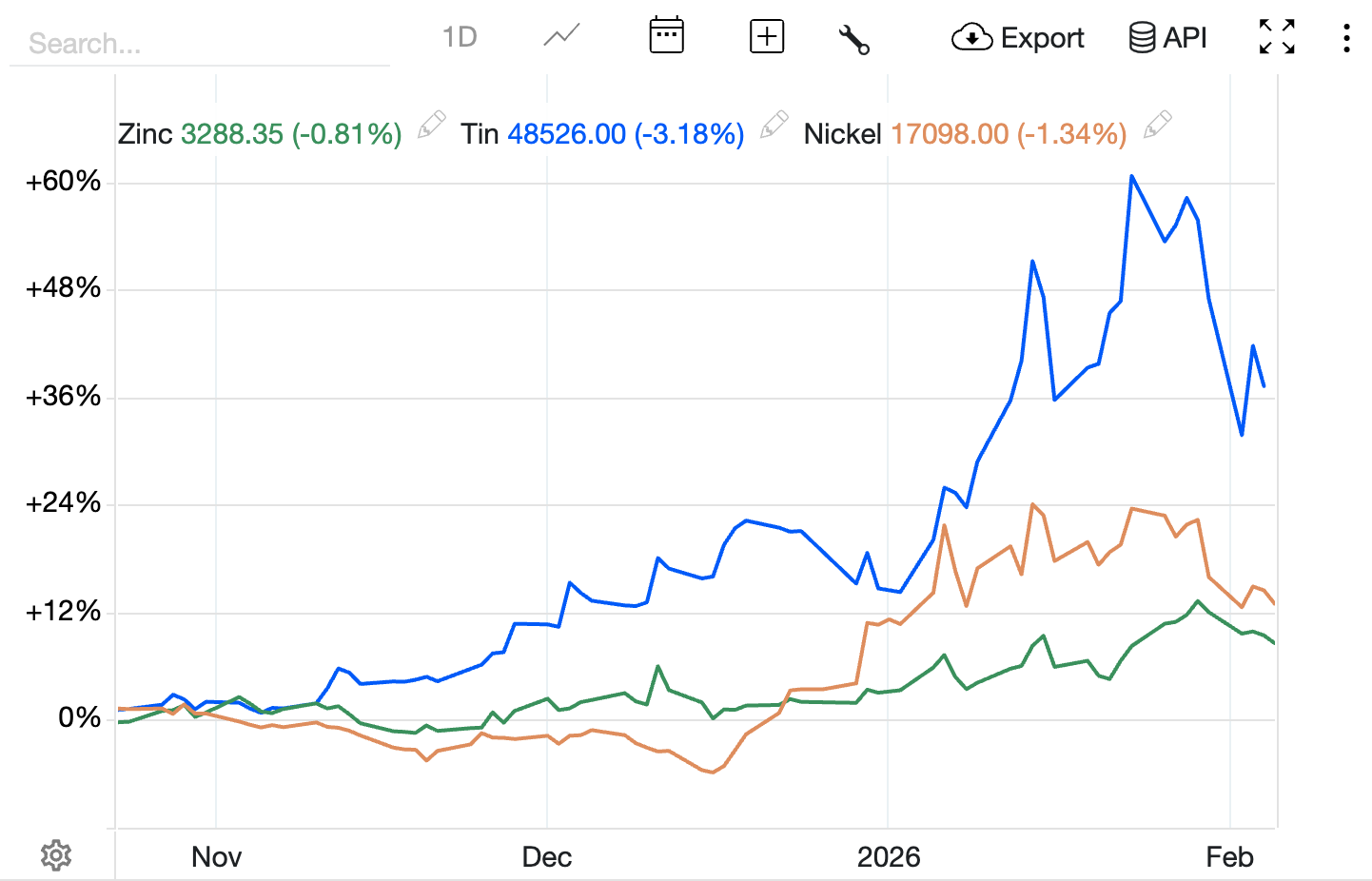

To provide a more complete picture, we include below the recent performance of other base metals, where the strength in tin stands out in particular.

Source: Trading Economics.

Lithium and other critical minerals (rare earths, etc.)

In lithium and critical minerals (including copper), politics has become a central variable, with the administration of Donald Trump accelerating an explicit supply-security strategy in response to China, the dominant player across these value chains.

The United States is combining initiatives to build strategic reserves, public–private capital and regulatory instruments to reduce dependencies and strengthen autonomy in key raw materials. In this context, the scale of Project Vault, involving $12 billion, is particularly noteworthy.

Washington is also promoting the formation of an alliance with friendly nations around critical minerals, aimed at coordinating investment, securing preferential access and reinforcing supply chains. Within this framework, price floors and special tariffs have been discussed. (We recommend this analysis for a deeper dive into these geopolitical dynamics.)

As for lithium, the price rally was very intense, as was the subsequent correction from the highs, consistent with the highly vertical nature of the preceding move. The upside leg was driven by news from China related to the battery value chain, particularly the possible withdrawal of export tax incentives, which the market interpreted as a signal of tighter control and potential strain on global supply, albeit with an indirect impact on lithium itself. This was reinforced by renewed demand narratives, especially those linked to energy storage (BESS). Once these expectations were priced in, and in the absence of fresh catalysts, the market corrected through profit-taking and technical normalisation, amid a broader increase in caution across commodities.

Fuente: Trading Economics.

With regard to Sigma Lithium, the lithium producer analysed in our first published report (and available to all readers), the company has recently released interesting updates, which we have been discussing in our community’s private forum.

See our report on Sigma Lithium

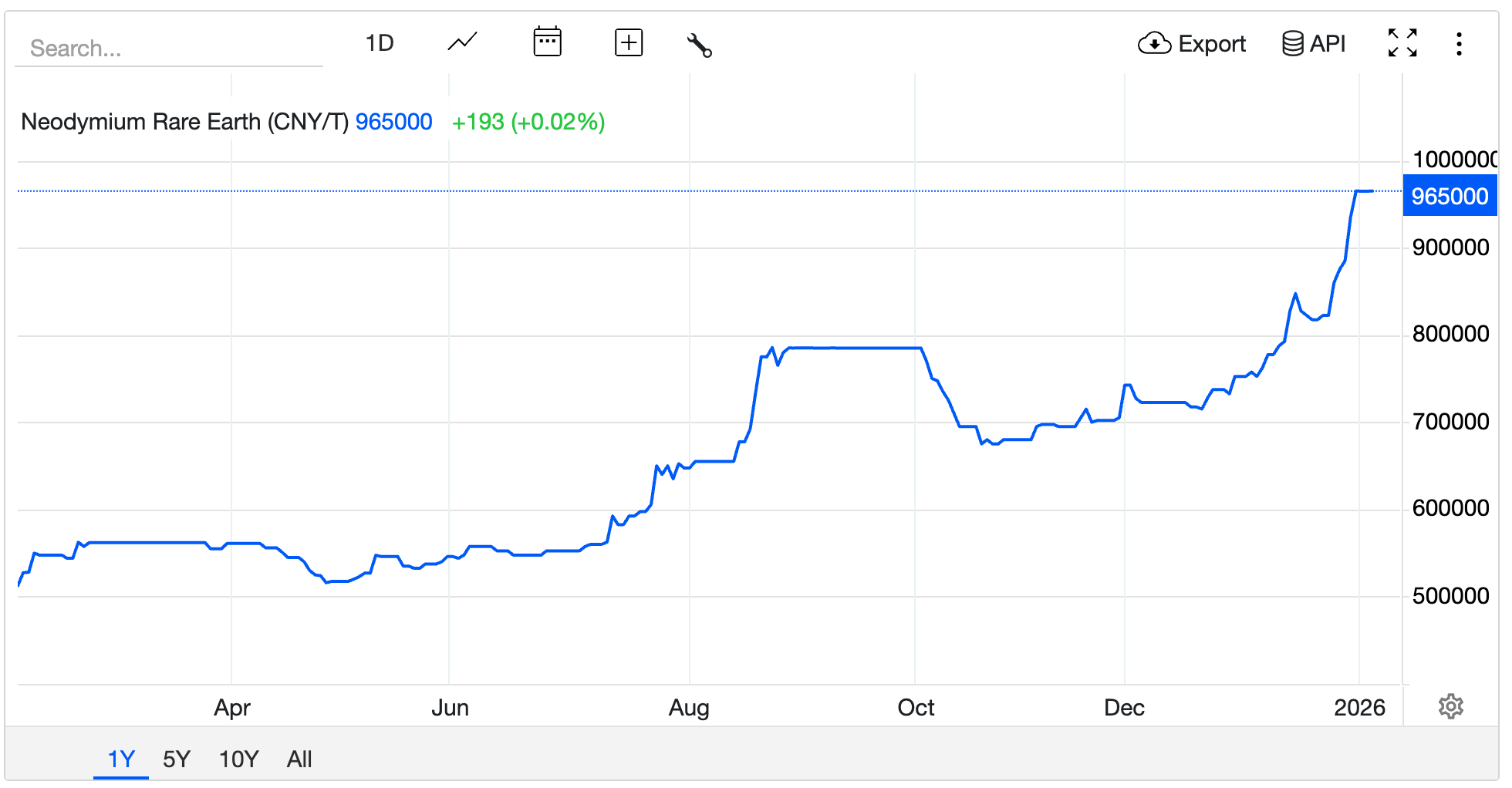

At the same time, light rare earth elements have also recorded a significant upward move, with NdPr standing out in particular (an alloy of neodymium and praseodymium used in permanent magnets for electric motors and other strategically relevant sectors such as electronics and defence). Unlike other markets, momentum in this segment remains strong.

Source: Trading Economics.

Uranium

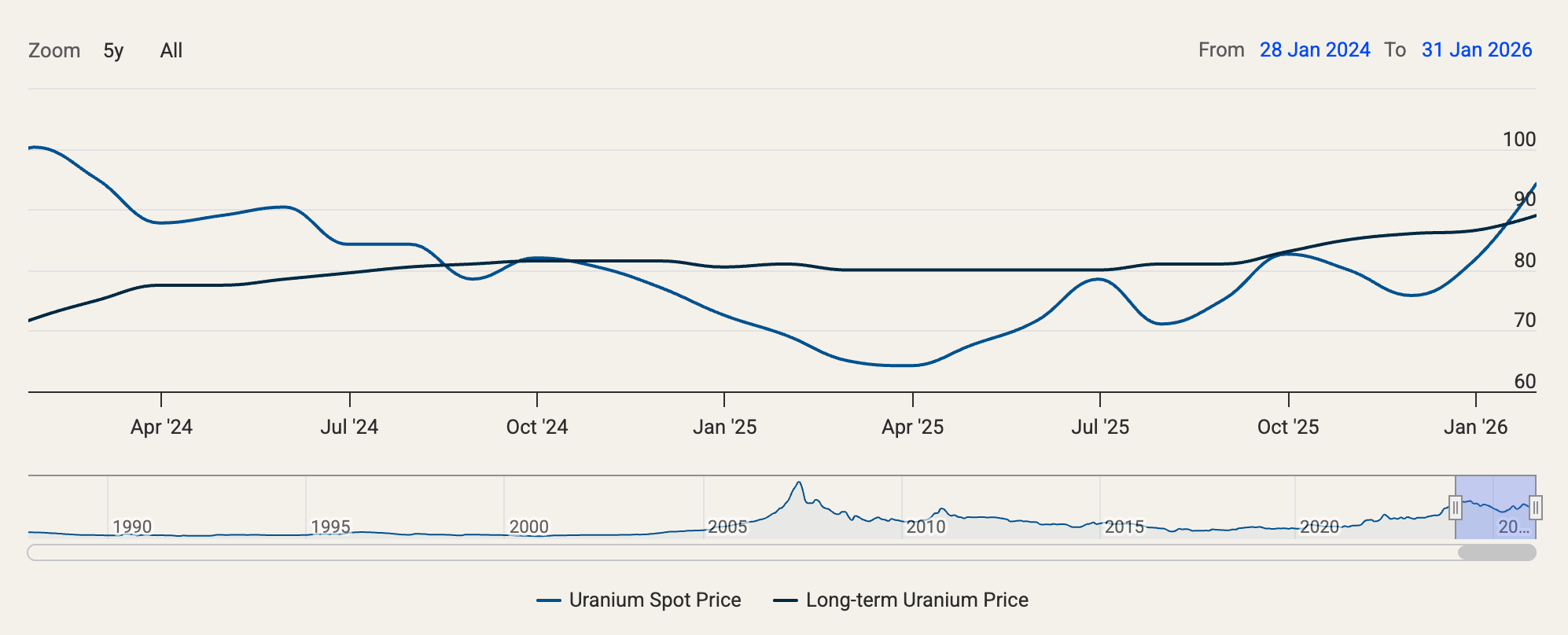

Uranium continues to display a structurally bullish underlying trend, supported by factors such as growing nuclear energy demand, supply security concerns and renewed interest in advanced reactor technologies, against the backdrop of a structural deficit expected to persist for many years.

Source: Cameco.

In the short term, however, volatility has returned to the spot market, largely driven by the activity of the Sprott Physical Uranium Trust (SPUT). A recent capital raise of more than $200 million in a single day enabled significant purchases of physical material, pushing spot prices above $100 as traders anticipated SPUT’s buying activity. This was followed by a correction, with prices retreating back toward the $90 level.

We conclude with the following table, which shows the returns of different sector-focused mining ETFs across various metals and time horizons, illustrating the high recent volatility discussed throughout this newsletter:

Source: Investing.com as of Feb 5 (before the North American open).

Additional resources

Charts of the month

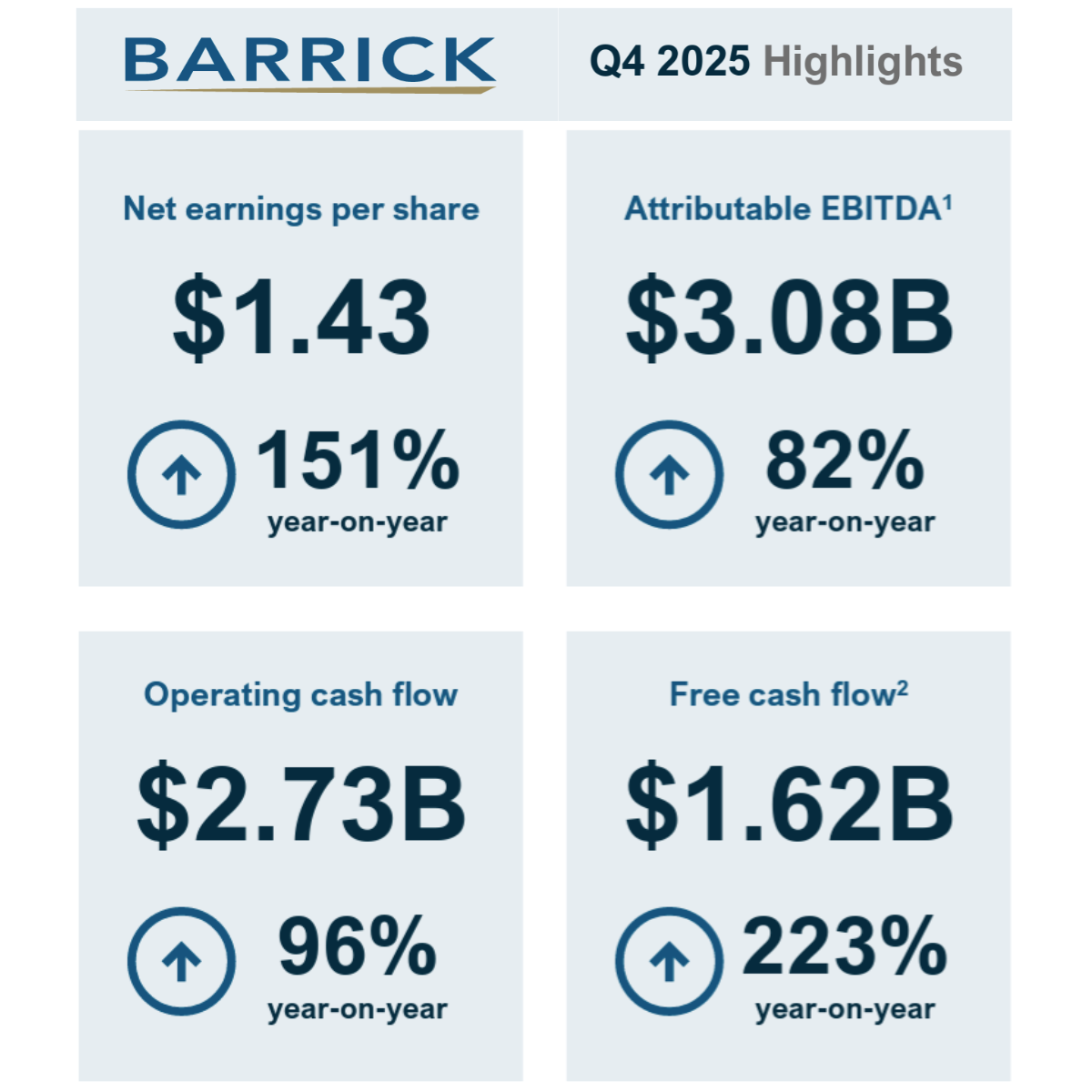

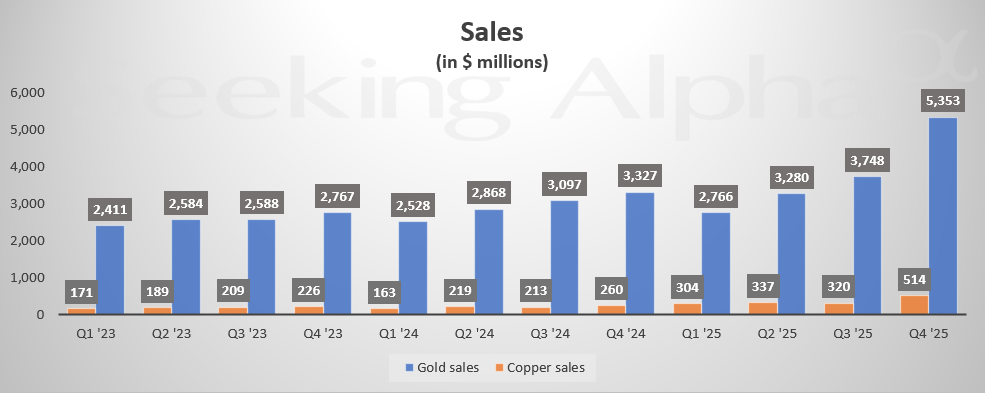

Growth in Barrick Gold’s financial metrics in its Q4 2025 results

Source: Barrick Gold.

Source: Seeking Alpha.

The results of Barrick Gold, one of the world’s leading gold producers, are illustrative of the spectacular year-on-year growth in financial metrics currently being delivered across the sector as a result of elevated gold prices. It is worth noting that the average gold price stood at $4,135 per ounce in Q4, and just under $3,500 for full-year 2025, compared with current prices well above $4,500, after briefly touching highs above $5,600 on January 29. As a result, barring a sharp and sustained decline in gold prices, this environment represents a strong tailwind for gold miners, which should continue to report significant growth in revenues and earnings.

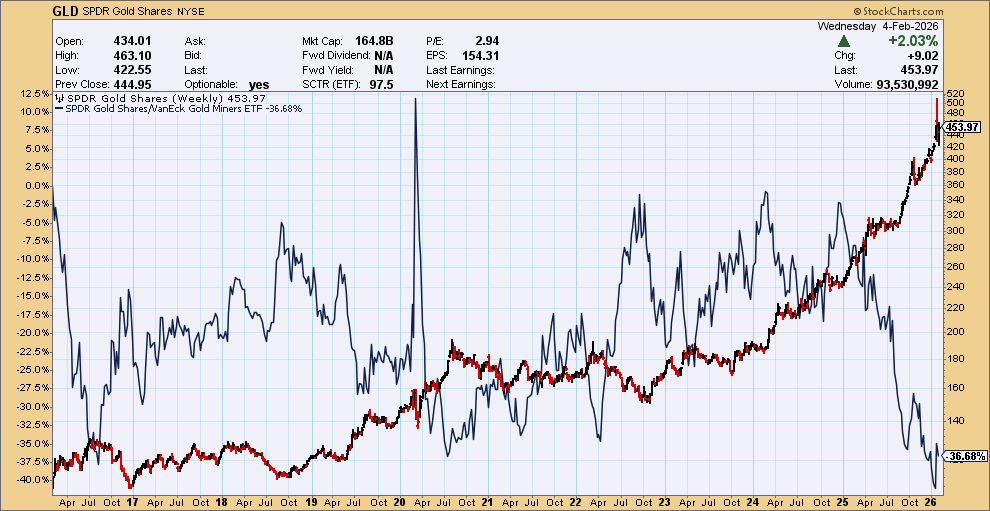

In this context, we believe it is useful to share the following chart, which plots gold prices (via the GLD ETF) in candlestick format alongside the gold (GLD) / gold miners (GDX) ratio, illustrating how this relationship has fluctuated over time.

In particular, the chart highlights how 2025 was a year in which rising gold prices translated exceptionally well into gold mining equities (a declining ratio indicates that miners outperformed gold).

Recommendations

We remain focused on precious metals, as recent market action makes this segment particularly relevant at present.

Video recommendation 1

We recommend the following interview with David Finch, a fund manager specialising in the mining sector, recorded in mid-January with gold trading slightly above $4,500. The interview contains several insightful observations, but in essence, Finch argues that the bull market in gold and mining equities is still at an early stage. He suggests that the gold mining sector could double in 2026 even with only a moderately higher gold price, driven by a valuation multiple expansion that has yet to materialise. He also argues that setting a specific price target for gold is of limited value given its monetary nature, and that the focus should instead be on the structural drivers of demand, including sovereign debt, fiat currency debasement and geopolitics. With institutional positioning from large capital allocators such as pension funds still low, and fundamentals remaining very strong across both precious metals and other metals such as copper, he warns that the biggest mistake of the cycle may be selling too early.

Video recommendation 2

We would also like to highlight this interview with another long-standing industry veteran, Adrian Day, recorded prior to the most recent parabolic leg higher in precious metals. He emphasised that even in bull markets, deep corrections are inevitable, and noted that there had still been no manic phase in gold and silver driven by massive capital inflows, suggesting that the top of the cycle remains some distance away. He also cautioned against one of the most common current mistakes: buying lagging mining stocks purely on the basis of price performance, assuming they will outperform leaders, without conducting rigorous analysis into why those stocks have lagged in the first place.

With this, we conclude the third edition of the Truth Below Ground monthly newsletter. We would greatly appreciate your feedback through whichever channel you prefer (links below, or simply reply to this email), not only on this newsletter but also on the reports we have published and the broader Truth Below Ground project. We look forward to hearing from you.

See you next time.