We kick off 2026 after a particularly intense year-end, both in metal markets (the core focus of this newsletter) and in the evolution of the Truth Below Ground project itself. Over the past few weeks, we have published two reports that clearly reflect our approach: a comprehensive analysis of Sigma Lithium, focused on the company’s technical, operational, and execution risks alongside its potential, and a macro-sector report on the copper market, where we assess the future balance between supply and demand from a structural perspective.

Our work and launch have also been covered by specialized media such as Funds Society, Mining IR, and the Money of Mine newsletter, reinforcing our commitment to independent, rigorous analysis.

Looking ahead to the coming weeks, we are finalizing our first members-only report, dedicated to NGEx Minerals, which will mark the beginning of a new phase for a project that aims to go beyond the easy and superficial narratives that often dominate the mining sector. Will you miss it? We invite you to learn more about how to become a member and what you will gain from it, and please feel free to reach out with any questions.

Without further delay, let’s dive into the most relevant developments of the past month, which has been particularly eventful. We have witnessed strong rallies across major metals, both precious and industrial, combined with rising volatility toward year-end and price moves that are far from common. Let’s get started.

Macro environment

A still supportive backdrop, with equity indices at record highs.

We begin with a snapshot of the global macroeconomic environment. In this edition, we do not revisit in depth some of the major structural themes already discussed in the previous newsletter (such as dollar depreciation, the “debasement trade,” or demand for real assets in an increasingly fragmented geopolitical landscape). Instead, we take that framework as given and focus on the key forces currently shaping the macro backdrop and helping to interpret recent moves in metals.

At a global level (and oversimplifying, given the divergences across regions), economic growth remains resilient, supported by a combination of looser monetary policies and expectations of further rate cuts, with particular attention on the Federal Reserve given its influence on the dollar. This is complemented by a greater willingness to use fiscal policy in a more expansionary manner. Inflation has remained relatively stable, helped by contained oil prices and a cooling labor market in the United States. That said, inflationary pressures could re-emerge, partly driven by rising costs linked to higher commodity prices, such as copper (already a reality), or oil should crude rebound after absorbing the supply increases implemented by OPEC during 2025.

One-year performance of U.S. equities (green), the dollar (ochre), and oil (red)

(Click on the images to enlarge)

(Click on the images to enlarge)

Against this backdrop, and now moving into 2026, geopolitics has taken on even greater importance. This is evident not only in the Trump administration’s intervention in Venezuela and the capture of Maduro, but also in the unrest unfolding in Iran, a significant oil producer and a key actor in an already fragile region. In the case of Venezuela, the ultimate motivation remains difficult to interpret and can hardly be explained solely through the lens of oil. Some analysts argue that a narrative centered on energy flows is incomplete (among other reasons due to the severe deterioration of the country’s productive capacity) and suggest that the operation is better understood as part of a longer-term strategic agenda related to security and global power dynamics, particularly the containment of China’s influence over critical resources, with additional implications involving Iran and Russia’s presence in the region.

Overall, we are facing a highly combustible environment. This geopolitical dimension, tied to the need to secure access to critical minerals and taking on a particularly broad and interventionist character under the Trump administration (as suggested by the chart below), is likely to remain a defining force for the macro outlook and commodity markets throughout 2026.

Similarly, markets will continue to be influenced by the artificial intelligence narrative, which is acting as a cross-cutting catalyst, boosting capital-intensive sectors and, by extension, demand and investor interest in certain metals and commodities linked to energy infrastructure, electrification, and data-processing capacity. Some view this as a bubble destined to burst sooner or later, dragging associated sectors down with it, while others see it as the early stages of a megatrend. Time will tell.

Metals and commodities

Explosive and highly correlated moves. Time for caution?

Gold and silver

If last month we devoted more attention to explaining gold’s price gains in 2025, this time the focus necessarily shifts to silver and the explosive nature of its recent move, which has resulted in sharp volatility in both directions. For now, corrections are being bought, suggesting the presence of an underlying bullish fundamental base. That said, this is not an environment in which to chase prices by jumping onto momentum.

Three-month performance of gold (ochre), silver (grey), and platinum (green)

Silver is trading close to $80 and closed 2025 with a gain of nearly 150%, driven by an unusual combination of factors: structural supply deficits, solid industrial demand over recent years (increasingly linked to uses such as solar energy), and perhaps the key driver behind its 2025 performance, a renewed monetary and financial interest, especially following gold’s strong run and the search for relatively cheaper monetary metal alternatives. The supply structure, largely dependent on by-product production from other metals, limits the market’s ability to respond even to significant price increases, although at these levels incentives are beginning to emerge for metal to enter the market from inventories and other sources.

Short-term catalysts have added fuel to this backdrop, including the Federal Reserve’s dovish stance in December and the announcement and market reaction to China’s decision to restrict silver exports from January 1, 2026, which has contributed to heightened speculative fervor (though some analysts view this reaction as unjustified). In such an environment, the combination of strong physical demand and certain dynamics in derivative markets tends to amplify price moves, an effect that becomes more pronounced during periods of low activity, such as the weeks around the Christmas holidays, when trading volumes and market depth decline.

In an effort to contain this extreme volatility, the CME (Chicago Mercantile Exchange, the leading derivatives market for commodities and precious metals) has raised margin requirements several times, forcing a reduction in leveraged positions. At the same time, the annual rebalancing of major commodity indices has taken place, generating mechanical selling following silver’s strong relative performance. These are largely technical dynamics, but they can exert downward pressure on prices in the short term.

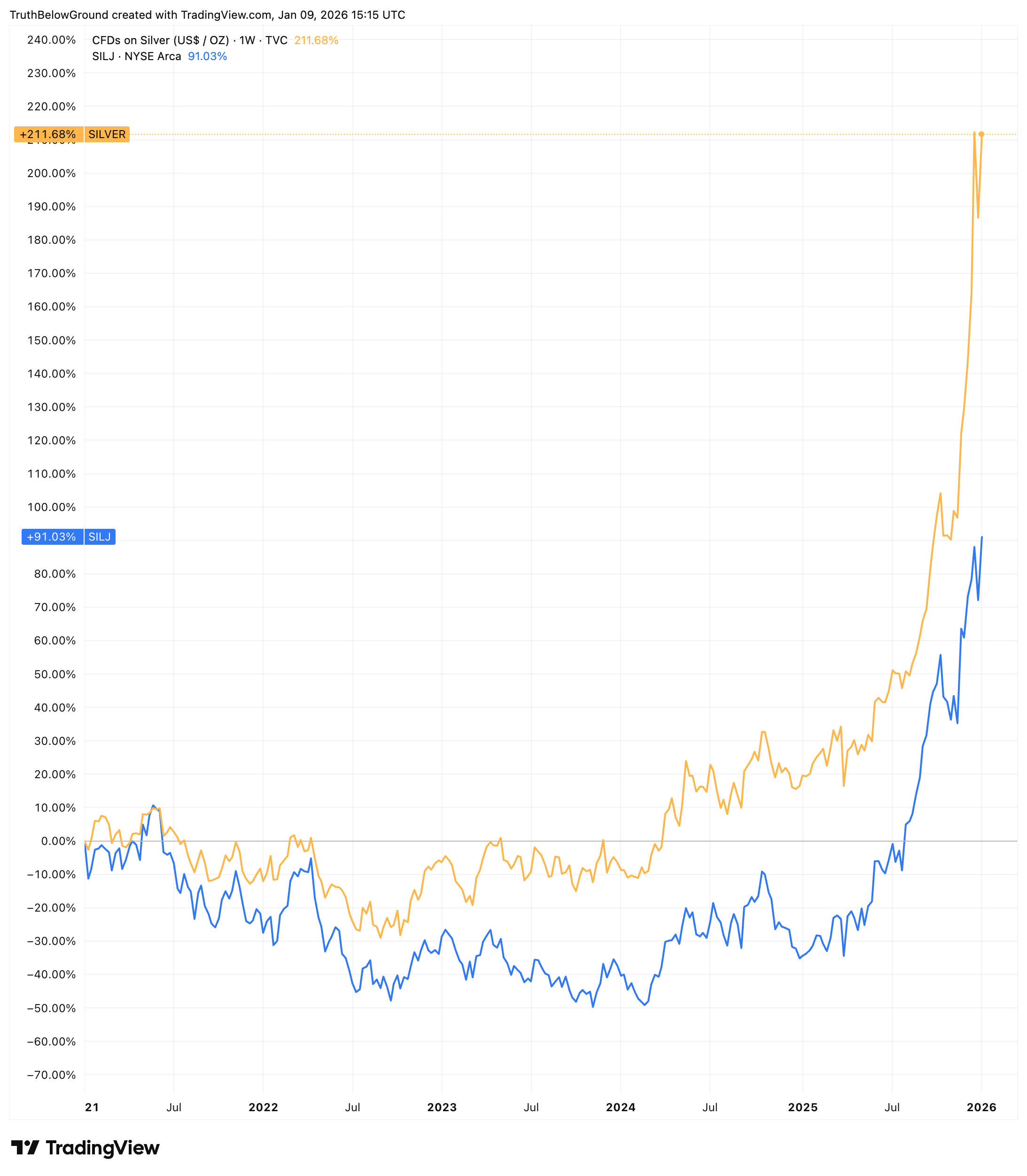

Despite silver’s explosive rally, silver mining equities (which are theoretically leveraged to the metal price due to operating leverage inherent in their business models) have posted relatively “modest” gains compared to the metal itself, as can be shown in the chart below going back 5 years where we can see the metal has outperformed the miners. This divergence may reflect a degree of market skepticism regarding the sustainability of current silver prices.

Silver (ochre) versus silver miners ETF (blue), 5-year performance

Ultimately, as in any market following such a rapid and explosive rise, the risk of corrections increases substantially. These corrections, which can be quite violent, are necessary to cleanse excess optimism and positioning.

Platinum and PGMs

Platinum and the broader PGM complex have experienced similarly vertical moves, driven by a mix of factors comparable to those affecting silver, alongside elements specific to PGM markets. Given the relatively narrow nature of these markets, financial demand has also played an amplifying role, intensifying price moves once perceptions of relative scarcity take hold and attracting flows seeking alternatives within the precious metals complex.

Beyond these financial dynamics, the structural backdrop for platinum remains solid. A more nuanced regional and technological evolution in the automotive sector has supported demand for autocatalysts, particularly as hybrid vehicles are expected to gain share and internal combustion engines remain relevant for longer in some markets. This is reinforced by the expected softening of the EU’s 2035 combustion engine ban and strategic adjustments by certain manufacturers outside China. Taken together, these factors, alongside the broader precious metals rally, have been very supportive for platinum, albeit with the same short-term volatility seen across the metals complex.

Are you a company or an institutional investor in need of an expert, multidisciplinary, and independent evaluation of mining projects? We may be able to help. Contact us

Copper

Three-month copper performance

Copper has joined this broader environment of strength, trading at record highs amid a convergence of well-known dynamics. On the demand side, rising investor interest in real assets and strategic metals, combined with momentum from artificial intelligence and electrification, has strengthened expectations for future demand tied to power grids, data centers, and generation capacity. On the supply side, structural rigidity persists, with few new projects capable of coming online in the near term and significant exposure to operational and geopolitical disruptions, some of which materialized during 2025 (e.g. Freeport’s Grasberg mine).

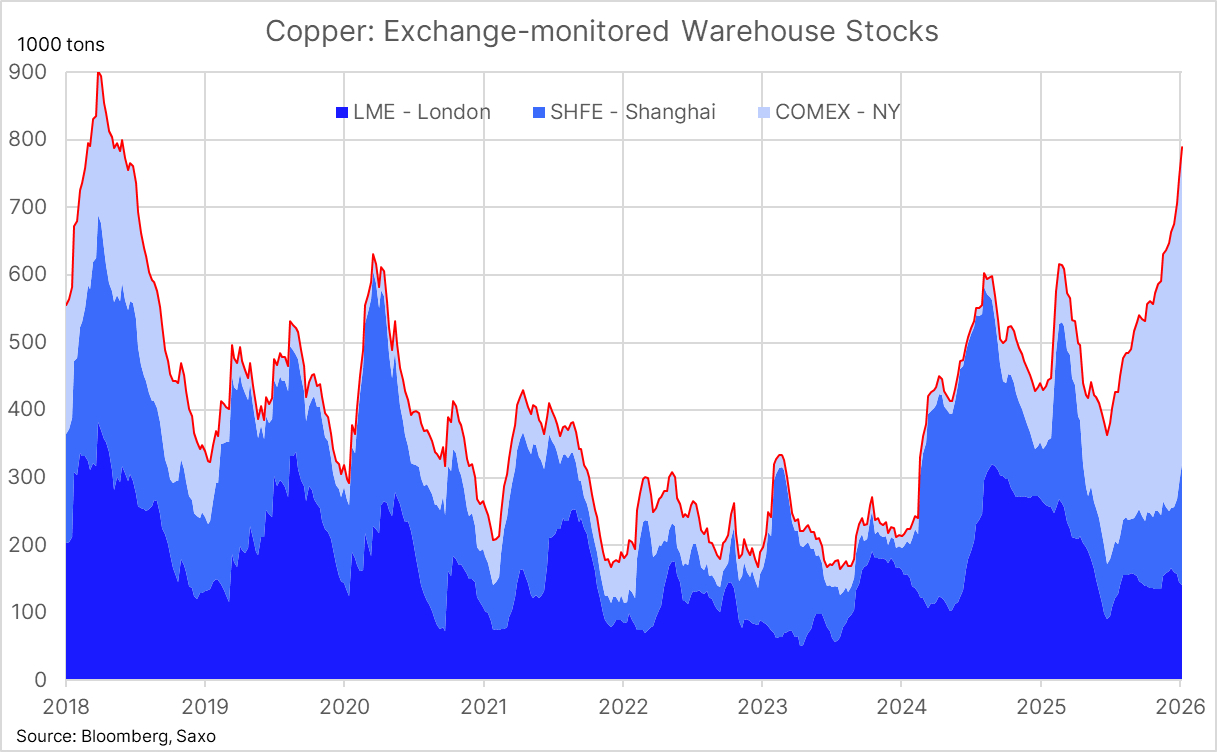

That said, in the very short term, signs are emerging that warrant a more cautious interpretation. Visible inventories tracked by major futures exchanges have risen to multi-year highs, with particularly strong growth in the United States, where the persistent threat of tariffs has encouraged shipments to COMEX, concentrating a significant share of global stocks there. At the same time, in China, elevated prices have begun to weigh on immediate industrial demand, as end users might be scaling back purchases amid difficulties passing on higher costs, leading to rising inventories and increased exports of refined copper. This combination raises reasonable questions about short-term price sustainability following a substantial rally over the past year.

Source: Ole Hansen

Nonetheless, beyond these short-term dynamics, the broader structural case remains intact, as discussed in our copper report. As with other metals, this positive long-term outlook does not eliminate the risk of near-term corrections after such strong gains.

>> Read our copper report

Lithium

Source: Trading Economics.

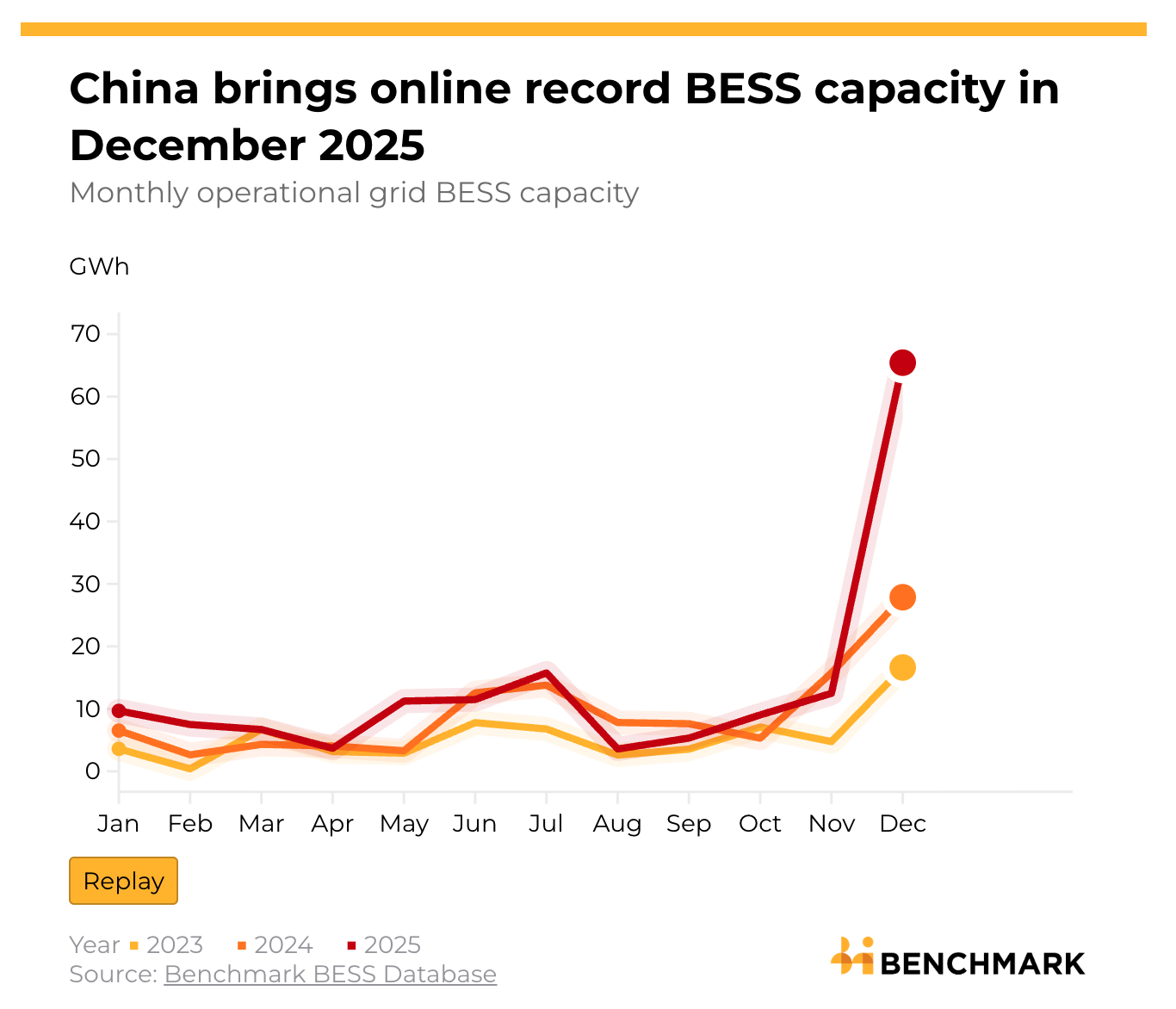

Lithium has continued to show clear signs of strength after bottoming following several years of oversupply and price pressure. The prior adjustment was deep and necessary, helping to eliminate excess capacity and marginal projects, and laying the groundwork for a more balanced market with room to recover. Beyond earlier supply-side restrictions (including the case of Sigma Lithium, whose production remains halted, likely a casualty of low prices), the most important recent development has been the shift in demand structure and outlook, with rapid growth in battery energy storage systems (BESS) emerging as a new structural driver, led by China.

Despite these positive prospects, several risks could hinder a sustained new bull phase. Excessive price increases could undermine the economics of storage projects, while technological evolution (including alternatives such as sodium-ion batteries) introduces additional uncertainty. At the same time, projected supply growth could cap price recovery. In this context, discussions are emerging around the potential establishment of strategic lithium reserves in the United States, aimed at stabilizing the market and securing domestic supply, reinforcing lithium’s status as a critical mineral.

>> Read our report on Sigma Lithium

Uranium

Uranium ended the year showing quiet strength, with spot prices edging higher through December despite the typically low trading volumes of that period. More important than the spot price itself is the evolution of the long-term contracting market, which continues to trend upward and provides a more representative signal of the true supply-demand balance. The combination of still-limited contracted volumes (well below annual demand of roughly 200 million pounds), albeit rising through 2025, and a structural supply deficit raises the question of how prices will respond when utilities return to the market in greater force. This pressure could be amplified by financial demand through vehicles such as Sprott, which have been actively absorbing physical material in recent weeks.

In parallel, the U.S. government continues to support the nuclear fuel cycle, announcing a $2.7 billion package for the enrichment phase, with further measures to promote domestic mining likely to follow.

In this context, Cameco executive Grant Isaac has described the market as particularly vulnerable to shocks, given the lack of sufficient mobile inventories to act as buffers against disruptions (or “shock absorbers” in this own words), whether from the supply side (disappointments in major development projects) or the demand side (institutional investors via physical vehicles or sovereign reserve announcements). Take into account that his is a highly conservative industry, where security of supply is paramount.

Truth Below Ground, the mining investment community powered by a multidisciplinary team of industry professionals. Risk and opportunity analysis from a truly technical perspective. Meet TBG’s Team

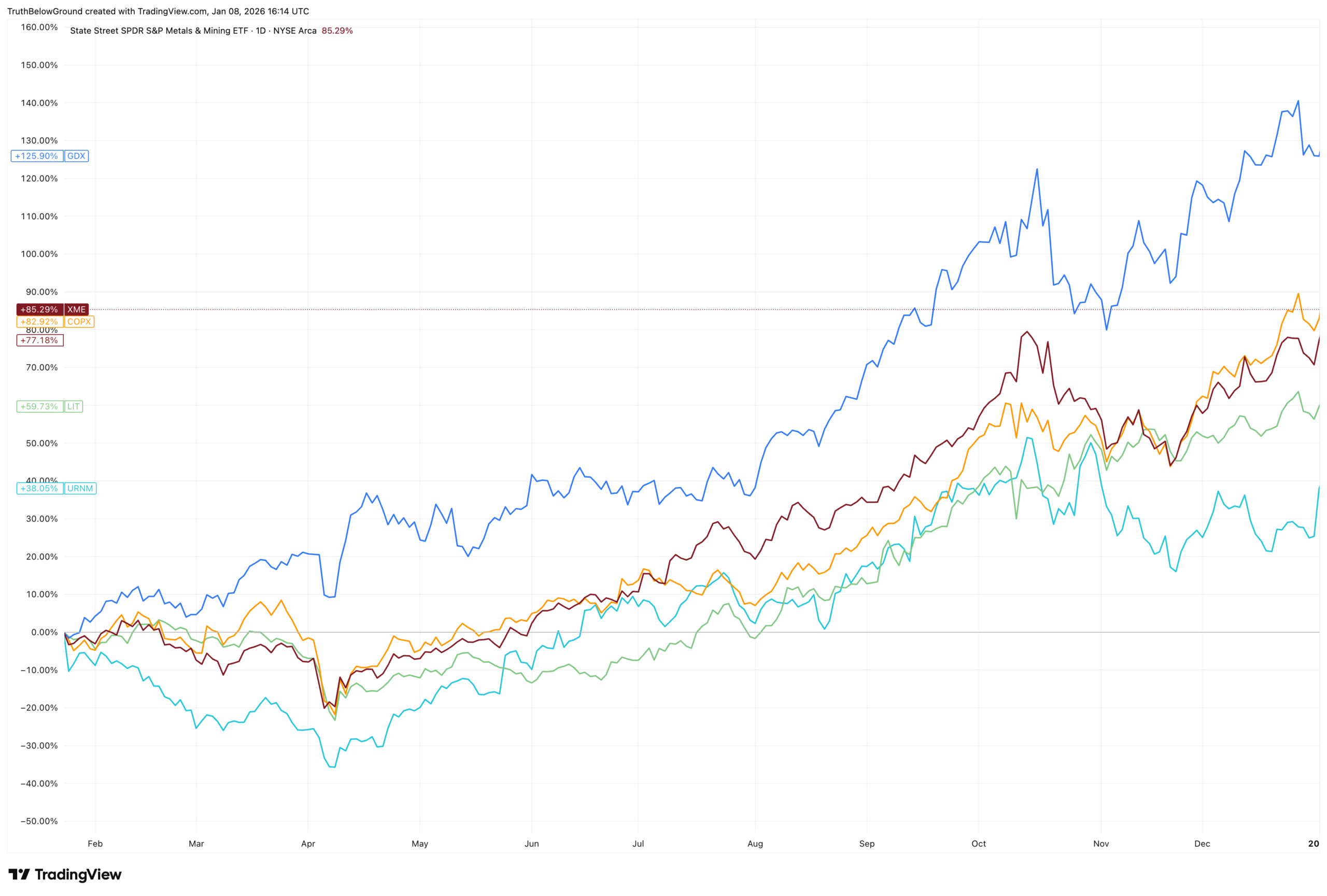

Finally, to close, we highlight the equity performance of different metals segments in 2025, with spectacular returns in gold and silver miners, the clear winners of the year. Copper miners were not far behind.

Note: GDX (gold and silver miners); XME (diversified materials); LIT (lithium); COPX (copper miners); URNM (uranium).

Additional resources

Chart of the month

Top-performing mining stocks of 2025, market cap above $1bn

Source: GoldDiscovery.

Building on the above, this month’s chart illustrates the magnitude of the rally in mining equities during 2025, particularly among companies with strong exposure to precious metals. Discovery Silver, Hycroft Mining, and Andean Precious Metals lead the ranking, posting extraordinary gains reflecting both operating leverage to metal prices and renewed capital flows into a historically underweighted sector that started from attractive valuations. The strong performance of larger, more institutional names such as Fresnillo is also notable, driven by silver’s move.

Looking ahead to 2026, it appears unlikely that such outsized and broadly based gains will be repeated across the precious metals sector. Much of the “easy money” may already have been made, shifting the focus toward a more selective and rigorous analysis, aimed at identifying opportunities that remain under the radar and distinguishing companies whose share prices have benefited from sector tailwinds without sufficient fundamental justification.

Recommendation of the month

We recommend this analysis with Michael Howell for its focus on liquidity and its implications across markets, including precious metals and commodities. Howell points to a potential shift in U.S. policy away from Wall Street-centric stimulus toward measures more focused on Main Street, with greater reliance on fiscal policy and low interest rates that support consumption rather than financial assets. The discussion highlights the difficulty of this balance, as withdrawing liquidity from financial markets without triggering stress is inherently challenging.

From a macro liquidity cycle perspective, the analysis connects to a particularly relevant idea for commodities: as the liquidity cycle approaches a peak and begins to turn, real assets and commodities tend to outperform, while equities often lose momentum. This is reinforced by liquidity impulses from China and a relatively constructive outlook for the real economy heading into 2026.

With this, we conclude the second edition of the Truth Below Ground monthly newsletter. We would greatly appreciate your feedback through whichever channel you prefer (links below), not only on this newsletter but also on the reports we have published and the broader Truth Below Ground project. We look forward to hearing from you.

See you next time.