[We share the fifth edition of our free monthly newsletter on the macro environment and natural resources investing that we send to our subscribers. Subscribe here]

Dear subscriber,

More than two and a half months have now passed since the start of the conflict with Iran, with the closure of the Strait of Hormuz as the main source of tension. Although there have been advances and setbacks in the negotiations during this time, a definitive resolution has yet to materialise. Meanwhile, implications and risks continue to accumulate which, judging by the new highs that equity markets keep reaching, the market appears to be partially overlooking. We already covered some of these factors in our previous edition, but it is worth updating them with the new information available in mid-May.

Before going into detail, we would like to remind you of our latest report on Savannah Resources, a London-listed company that owns the Barroso lithium project in northern Portugal and whose share price has appreciated strongly amid the recent rally in lithium prices. The report, in addition to evaluating risks and opportunities across the most relevant areas (geology, mining, metallurgy, ESG and regulation, management team and finances), includes a valuation sensitivity analysis under different scenarios.

Access the Savannah Resources Report

The report is available both to community members and as an individual purchase.

We would also like to share a new section on our website dedicated to presenting the analytical methodology we apply across the different companies we cover:

Without further delay, let us attempt to summarise the most relevant developments in the macro and metals environment.

Macro environment

Equity markets at record highs and the risk of an energy crisis: pure complacency or some genuine foundation?

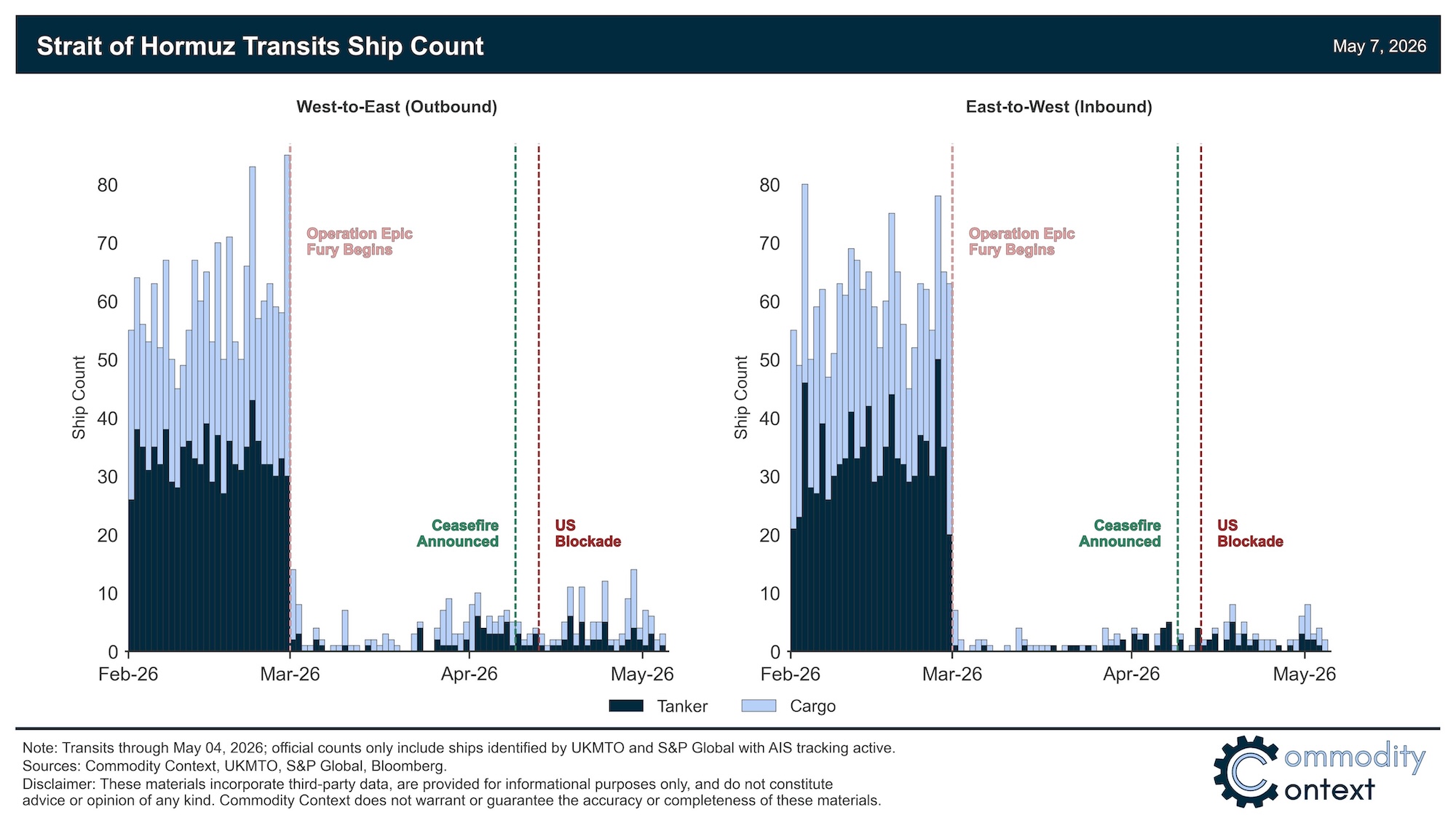

The conflict between the United States and Iran has now exceeded ten weeks and has triggered one of the largest disruptions to global energy supply in history. The Strait of Hormuz (through which roughly 20% of global seaborne oil trade transits) has been effectively closed or severely restricted since March, with no meaningful progress.

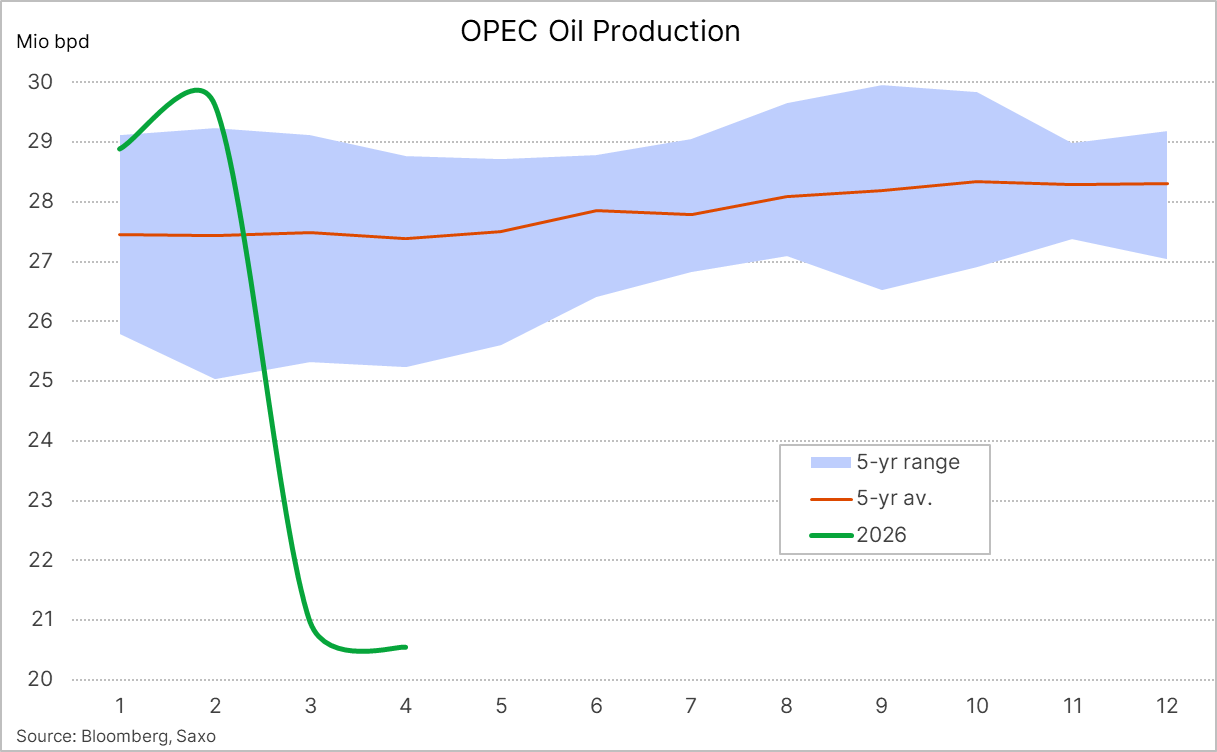

In this context, oil production from Gulf countries has collapsed. The oil price, however, has shown some containment, moving volatilely in response to the latest headline, on the hope that negotiations will lead to an agreement that ends the strait’s closure.

Source: Ole Hansen

Despite this backdrop, US equities have rebounded strongly and surpassed previous highs. The explanation can be found across several factors.

First, it is important to remember that financial markets are processes of discounting expectations — that is, they are forward-looking. No matter how negative the past or even the present may be, if they discount a more positive near-term future, they will behave favourably. In this case, markets appear to be already pricing in a near-term reopening of the strait without significant additional friction.

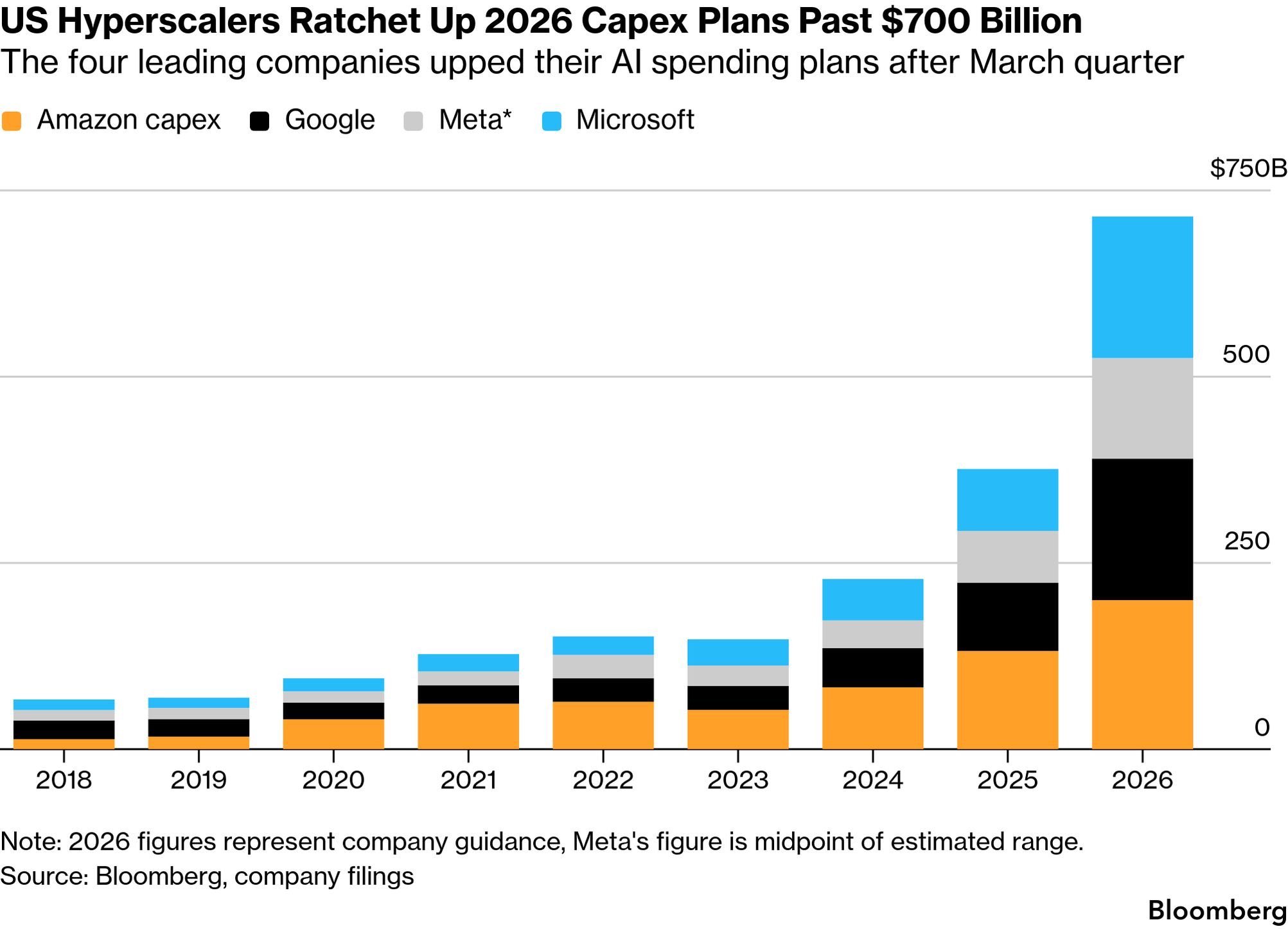

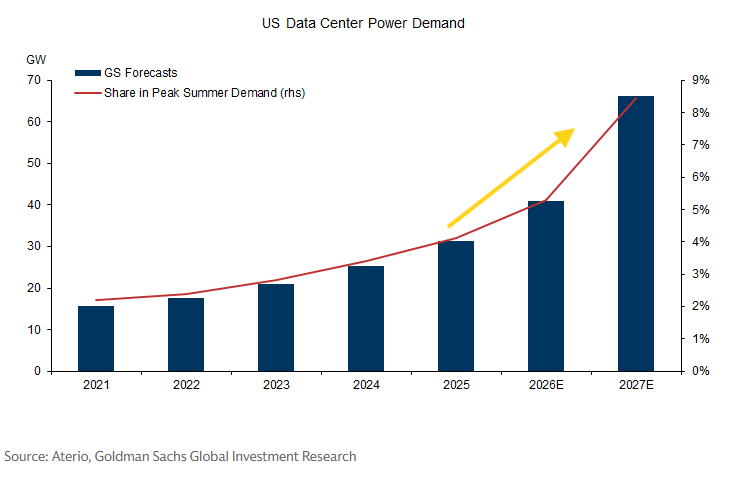

Adding to this expectation is the strength of corporate earnings, driven by technology, semiconductors and sectors related to the extraordinarily strong AI capex cycle and the development of the surrounding infrastructure (notably investment in data centres). This phenomenon, which is also contributing positively to US economic growth, is led by the so-called hyperscalers:

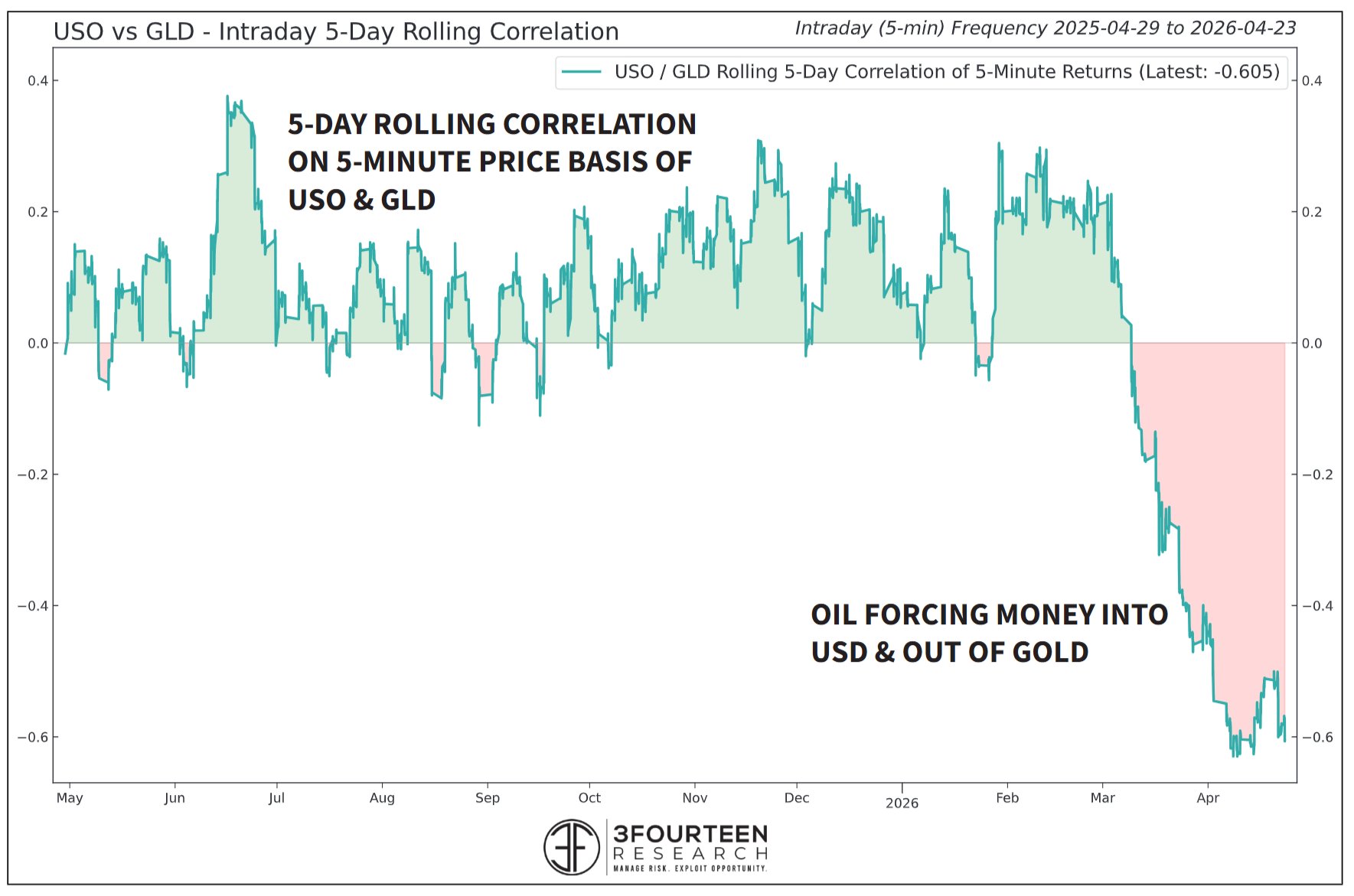

The oil market: a thermometer of market positioning?

Returning to the earlier point about market expectations of a favourable and near-term resolution to the Hormuz conflict, this same logic also explains why oil prices, despite the shock, are not higher.

As one sector trader and analyst noted, Asian oil buyers are currently breathing easier, having received cargoes purchased in the panic of the early stages of the conflict, while China is rumoured to have been releasing barrels from its strategic reserve. The question for physical market participants has shifted: it is no longer “where do I get barrels now?” (as it was at the start of the conflict, during the panic phase), but “if Hormuz reopens, will we not face a physical oversupply?”. This forward-looking reading keeps prices contained, in a context of wait-and-see attitudes among traders, confident that the worst-case scenario will not materialise.

The risk, however, is worth keeping in mind: according to specialised sector analysts, even if Hormuz were to reopen today, supply would not normalise easily or quickly. The region’s energy infrastructure has sustained damage that requires months of repairs, production interruptions do not resume overnight, insurance and freight will remain elevated for a prolonged period, and global inventories have drawn down very significantly and could continue doing so to dangerously low levels. If reality does not change in the very short term, the apparent calm of the market (both oil and equities) could turn into another episode of broad-based selling, a repetition of the dynamics already seen in March and which we detailed in the previous newsletter.

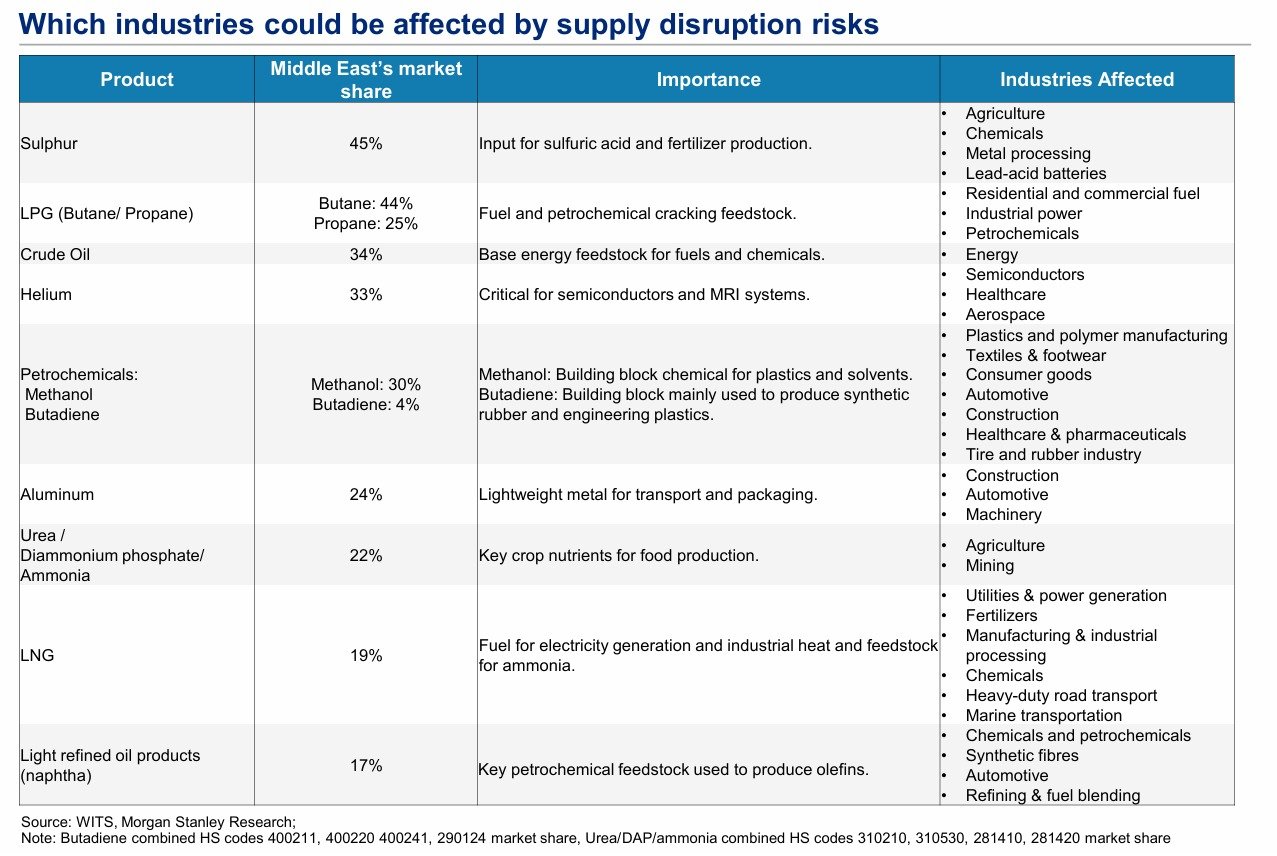

A similar scenario could develop in other industries that act as a critical input for very different areas of the economy, something we will discuss further below. On this point, we share again the same chart we already presented:

Metals and commodities

Gold maintains its positive correlation with risk assets; supply disruptions push copper and other base metal prices higher

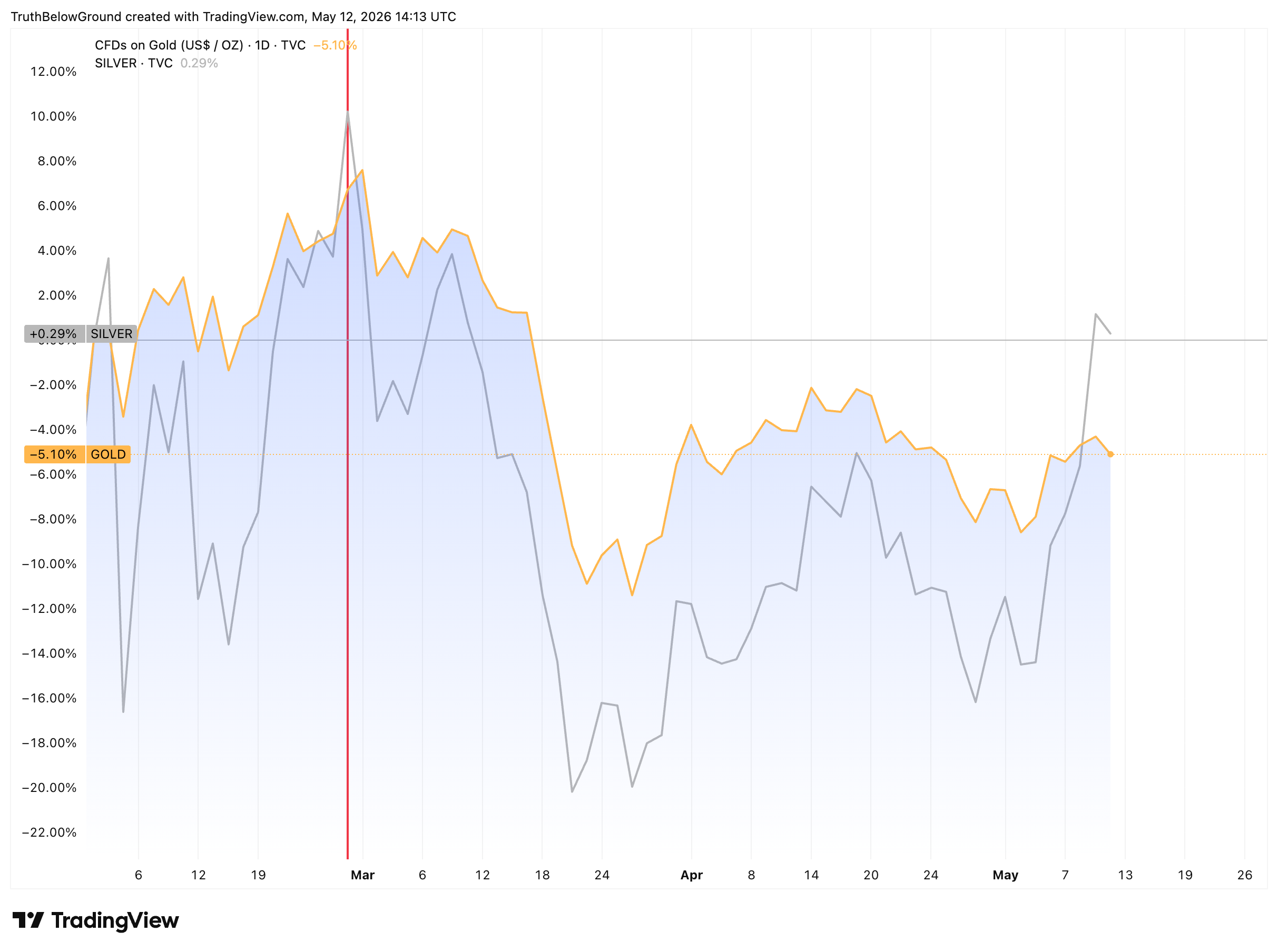

Gold and silver

In the macro scenario we have outlined, gold has continued to move as a procyclical asset following the news flow around the war with Iran, recovering only part of the earlier decline. Silver, by contrast, has bounced back much more strongly from its lows.

Performance in % of gold (orange) and silver (grey) over recent months

A chart that illustrates well the new regime in which gold is moving is the following, which shows the very clear negative correlation between the price of gold and oil since the beginning of the conflict:

In other words, when oil rises sharply, reflecting a deterioration in news flow around the war, gold tends to fall, along with other assets such as equities and bonds, while the dollar rallies. And when oil falls on news or rumours about progress in negotiations, gold tends to rise, alongside equities and bonds, while the dollar weakens.

Here it is worth revisiting the hypothesis we presented in the previous newsletter: after 2022, the main driver of gold may have shifted from safe-haven demand or real rates to reserve accumulation by emerging market countries with trade surpluses. Under this reading, gold has become procyclical with global surpluses rather than inversely correlated with risk. If this hypothesis is correct, this clear negative correlation with oil should not be quite so surprising.

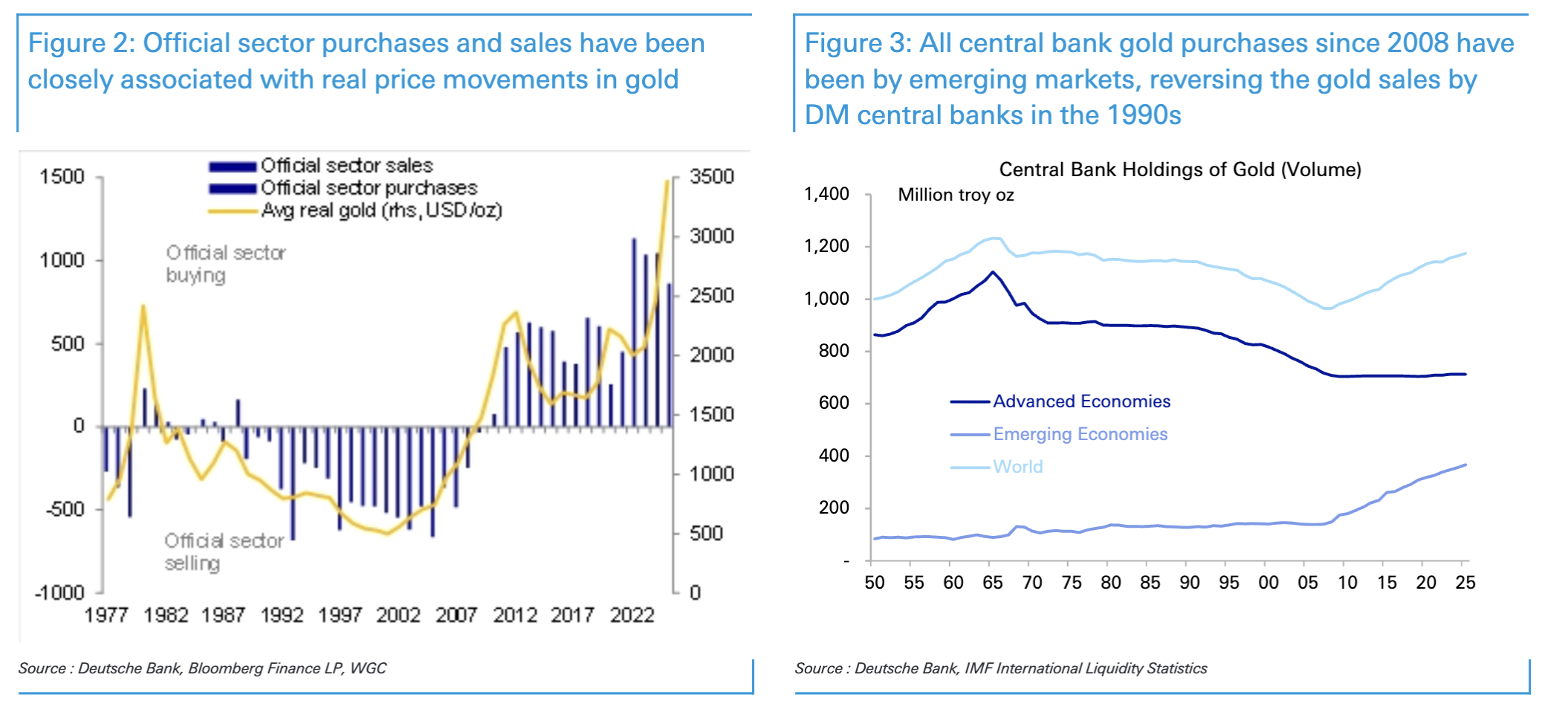

In this regard, the data confirm that emerging market central banks were net sellers of gold during the acute phase of the conflict, led by Turkey. The move is consistent with the fact that Turkey held a share of gold in its reserves above 60%, making it one of the few central banks with enough margin to use that asset as a source of liquidity. In moments of stress, gold ceases to be a reserve asset and becomes a source of liquidity, and that shift in function explains part of the recent price behaviour.

It is worth noting, however, that this episode does not appear representative of a broader trend among emerging market central banks. According to the same IMF data, countries such as Poland and Kazakhstan continued buying gold in March, and PBoC data shows the fastest pace of purchases in the past year. Most emerging market central banks hold a much lower share of gold in their reserves than Turkey, with significant margin to continue increasing it. In other words: the Turkey episode is real and has weighed on prices in the short term, but the structural thesis of gold accumulation by emerging market central banks, in a geopolitical context undergoing profound change, may remain intact.

Are you a company or institutional investor in need of an expert, multidisciplinary and independent evaluation of mining projects? We may be able to help.

Copper

Copper, despite warnings about rising inventories and macro uncertainty, has risen strongly in recent weeks. The move reflects resilient demand (especially in China) and a tight supply situation, with a news flow clearly favourable to the bullish side.

On the supply side, the most notable development has been the recent news from Grasberg. Freeport-McMoRan has announced that full capacity at the mine (the world’s second-largest producer) will be delayed until early 2028; the operation is currently working at 40-50% of capacity and 2026 production has been revised down significantly. This adds to the problems at Kamoa-Kakula and El Teniente, on top of the general weakness in Chilean production, leading analysts to project deficits in the copper market in 2026. Therefore, on top of a structural balance already tight by the chronic insufficiency of new projects relative to growing demand which we explained in our copper report, recent disruptions further widen the expected deficit.

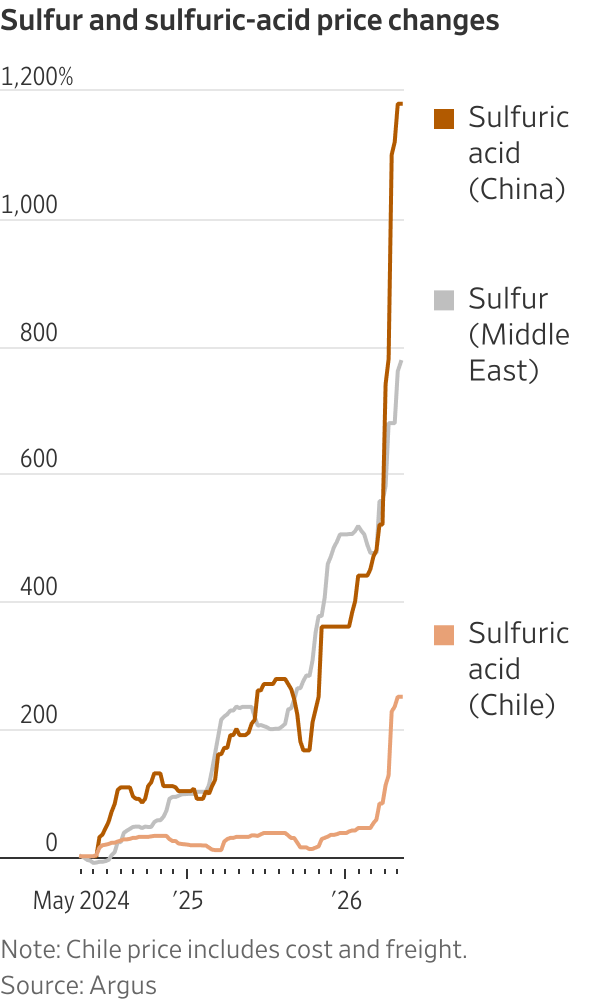

If that were not enough, we have to add to the equation the factor most strongly moving the value chain, not only of copper but also of other base metals such as nickel: sulfuric acid, whose implications we already outlined in the previous newsletter. The situation has deteriorated after China (the world’s largest exporter) communicated the halt of its exports starting in May, transferring an immediate shock to key importers such as Chile, Indonesia and the DRC. This is relevant because around 15-20% of global copper production depends on this input: these are the operations that, rather than going through the traditional route of smelting and refining, use leaching processes in which copper is extracted from the ore by dissolving it with acid. The final impact on global production remains to be seen, but at the very least the producers that depend on it will see their costs come under significant upward pressure, both via the acid itself and via more expensive fuel, as reflected in the recent results of Teck.

A brief technical aside is useful here to understand the most striking distortion all this has generated in the copper market. In the traditional copper production route (80% of total output), miners sell concentrate to smelters, which transform it into anodes, with sulfuric acid as a by-product. These anodes are then sent to refineries, which convert them into cathodes. For these processing and refining services, miners pay charges known as TC/RC (treatment and refining charges), which traditionally function as a barometer for the tightness of the concentrate market. Well, these charges have moved into negative territory, which suggests something peculiar: it is now the smelters paying the miners to secure the concentrate, because the most profitable part of their business has flipped. Copper cathode has become almost a by-product, while sulfuric acid (that traditionally secondary co-product) has turned into the product generating most of their revenues. See what Robert Friedland, CEO of Ivanhoe Mines (Kamoa-Kakula), had to say on the matter here.

Lithium

The price of lithium carbonate has now risen for several consecutive months and shows an outstanding bullish trend, having more than tripled from the lows of summer 2025. On the demand side, two vectors stand out: the strength of BYD’s international sales and the rest of China’s electric vehicle ecosystem, and the emergence of data centre operators as a new source of structural demand (their energy storage systems, BESS, require more lithium per unit than those used in electric vehicles, and the pace of deployment is accelerating in parallel with the AI capex cycle we have already referred to). We recommend this reading on Canaccord’s projections of a structural lithium market deficit by 2035.

Discover the Barroso lithium project in Portugal (Savannah)

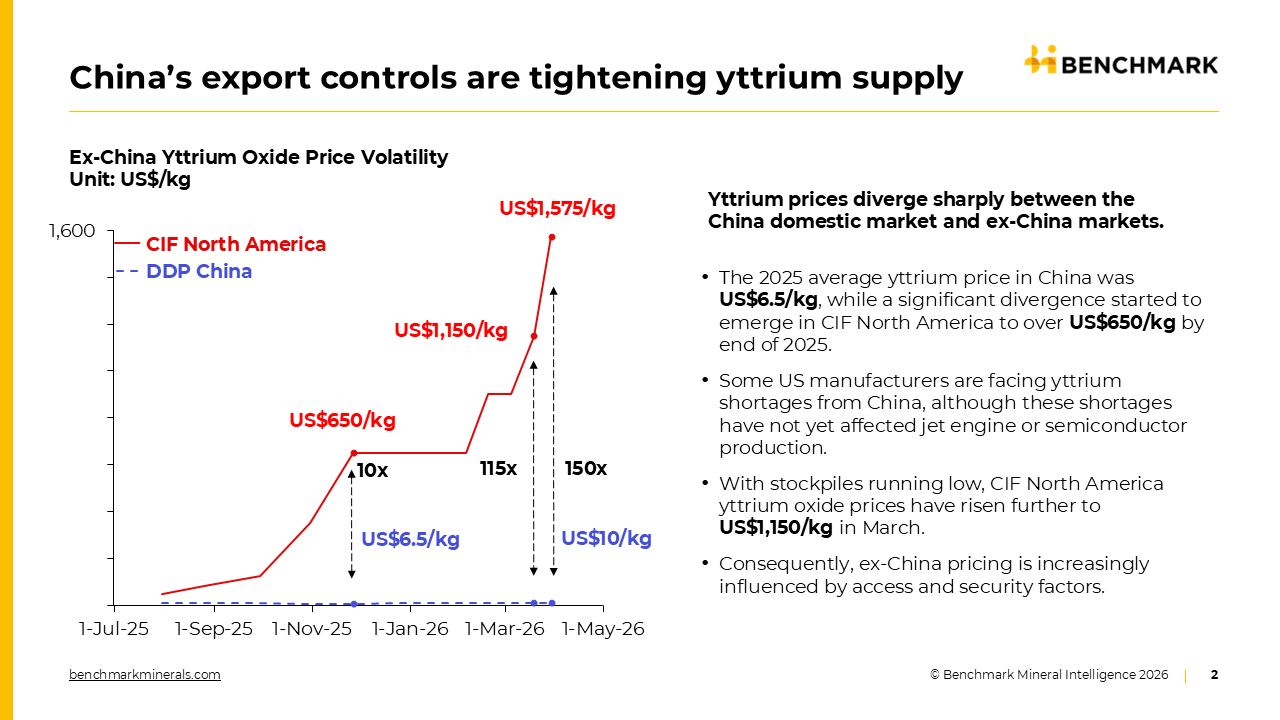

Critical minerals (rare earths, tungsten)

What is happening in this segment has little to do with the dynamics of a “free” supply-and-demand market, and much to do with geopolitics, with a global dual-price system (Chinese domestic vs. ex-China prices) that is consolidating as a structural feature given China’s dominant role.

An extreme case is yttrium: according to Benchmark Mineral Intelligence, the Chinese domestic price has barely moved from $6.5-10 per kilo between July 2025 and May 2026, while the North American price has gone from similar levels to $1,575 per kilo (a multiple close to 150x).

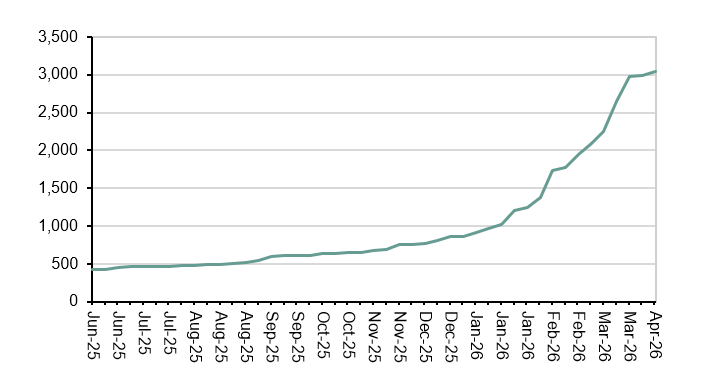

Tungsten illustrates the same dynamic, combined with a sharp tightening of supply and an acceleration of demand. According to Edison Group, the ex-China price of APT (ammonium paratungstate, the first commercially standard product in the tungsten value chain and therefore the sector’s benchmark) has moved from a five-year average of $300/mtu to approximately $3,000 (10x), in a context where China is tightening and legally consolidating its export controls. On the demand side, the main driver is the defence sector: tungsten is the material of choice for armour-piercing penetrators and high-velocity ammunition, in a context of accelerated consumption by the conflict in Iran and the need to replenish Western military inventories.

ex-China APT (ammonium paratungstate) price evolution, USD/mtu

Source: Edison

In parallel to these sectoral movements, several signals from China point in the same direction, with an explicit message: secure what it lacks (copper, iron, lithium, cobalt, nickel) and consolidate its dominance over what it already controls (rare earths, tungsten, tin). The reading is that China is building an institutional and legal framework that allows it to maximise its influence over prices and global supply of the most strategic minerals, a variable that the market is not yet fully discounting and at a moment when the West is decades and many steps behind China in the race to secure strategic supply.

Regarding uranium, prices remained relatively stable. Beneath that apparent calm, however, the structural thesis continues to gain strength. The supply side remains fragile, as illustrated again by the very short-term shock caused by the floods in Saskatchewan (Cameco temporarily suspended Key Lake and reduced activity at McArthur River after the collapse of the Smoothstone River Bridge), an episode that is not expected to have a material impact. On the demand side, Western utilities have yet to return in a sustained way to long-term contracting (the structural deficit of the next decade will not be covered without that return), hyperscalers are signing direct contracts with the nuclear sector to feed the insatiable energy demand coming from data centres (see chart below), and expectations around new nuclear capacity are accelerating.

Truth Below Ground, the mining investment community powered by a multidisciplinary team of industry professionals.

Mining sector

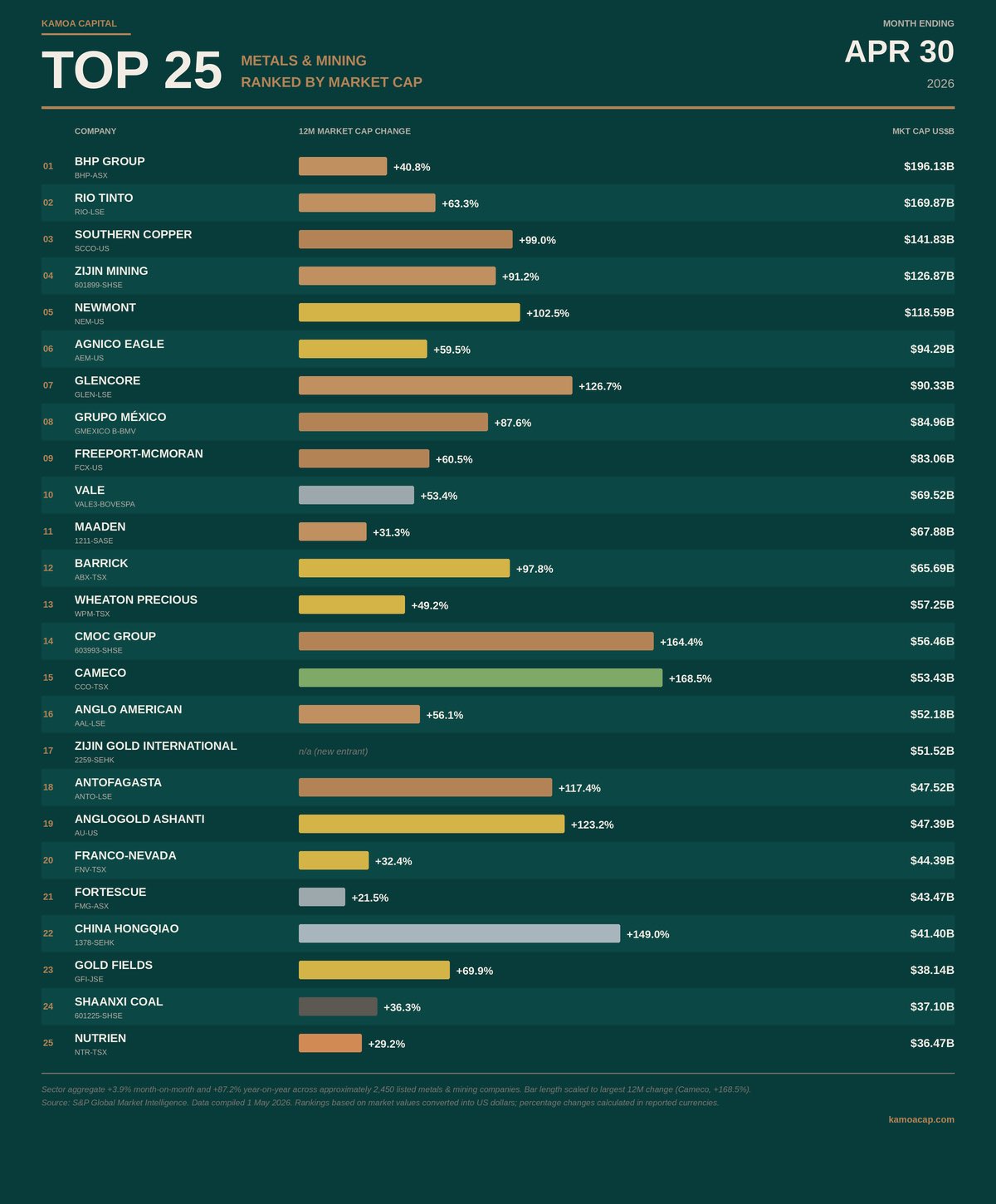

If in the previous edition we spoke of recent declines in the sector, in this edition the most relevant story is the substantial returns that the main mining companies of the world have delivered over the past twelve months. The following ranking compiled by Kamoa Capital (top 25 by market cap, as of April 30) illustrates the magnitude of the move, with Cameco (uranium/nuclear) leading the table with a rise of nearly 170%, reflecting the favourable change in expectations:

Source: Kamoa Capital

A similar picture can be seen across sector ETFs, where, compared to the table we showed in the previous edition (as of March 23, in the middle of the correction), returns have improved notably, particularly in junior silver miners and in the lithium and copper segments, in line with the moves in the underlying commodities:

| ETF | 1 week | 1 month | YTD | 1 year | 3 years |

|---|---|---|---|---|---|

| SPDR S&P Metals & Mining | +2.35% | +6.62% | +19.04% | +108.77% | +157.82% |

| VanEck Gold Miners | +4.92% | -1.58% | +12.20% | +106.99% | +183.78% |

| Amplify Junior Silver Miners | +10.98% | +7.46% | +23.85% | +184.87% | +225.76% |

| Global X Copper Miners | +11.26% | +6.77% | +28.03% | +128.92% | +140.22% |

| Global X Lithium | +0.26% | +12.48% | +38.11% | +131.23% | +42.19% |

| Sprott Uranium Miners | -4.67% | -7.27% | +16.38% | +69.26% | +100.88% |

Source: Investing.com, as of May 14, 2026.

This positive reading, however, should not overlook an important headwind that is starting to appear in company accounts: cost inflation in the sector, particularly that derived from the energy shock, which we already mentioned earlier in the case of Teck in Chile. The current earnings season is dimensioning the impact with more precision. Barrick Mining has quantified that, for every $10 change in the price of the barrel, the cost associated with diesel consumption rises by $12 per ounce across its gold operations and $0.04 per pound across its copper sites, all on a 2026 guidance built on a WTI assumption of $70 per barrel (a reference the market has been leaving behind for weeks). Newmont, the world’s largest gold producer, provides these figures: with Brent also assumed at $70 and diesel representing approximately 6% of direct operating costs, every $10 move in the barrel implies approximately $60 million of cost impact, equivalent to $12 per ounce in AISC. The company maintains its 2026 guidance despite inflationary pressures and breaks down its cost structure into approximately 50% labour, 30% materials and consumables, and 15% fuel and energy.

These figures should be read with a caveat: although the miners themselves are the most reliable source for calibrating the impact, they also have incentives to present it with a reasonably optimistic bias, and to direct costs one has to add second-order effects (salary pressure, freight, etc.) that materialise with a lag. The next earnings seasons will likely show upward revisions to AISC guidance and margin compression, especially for producers with less hedging on the energy component. In the medium term, however, the reading is that if the cost of extracting the marginal ounce of gold or the marginal pound of copper shifts structurally higher, the floor of metals prices should also shift higher.

This structural reading is starting to permeate institutional money too, as captured in a recent Reuters article titled “Big funds bet billions on mining supercycle”: capital flows into the mining sector have accelerated significantly, driven by AI infrastructure, increased defence spending, and the rotation from expensive technology into real assets.

Additional resources

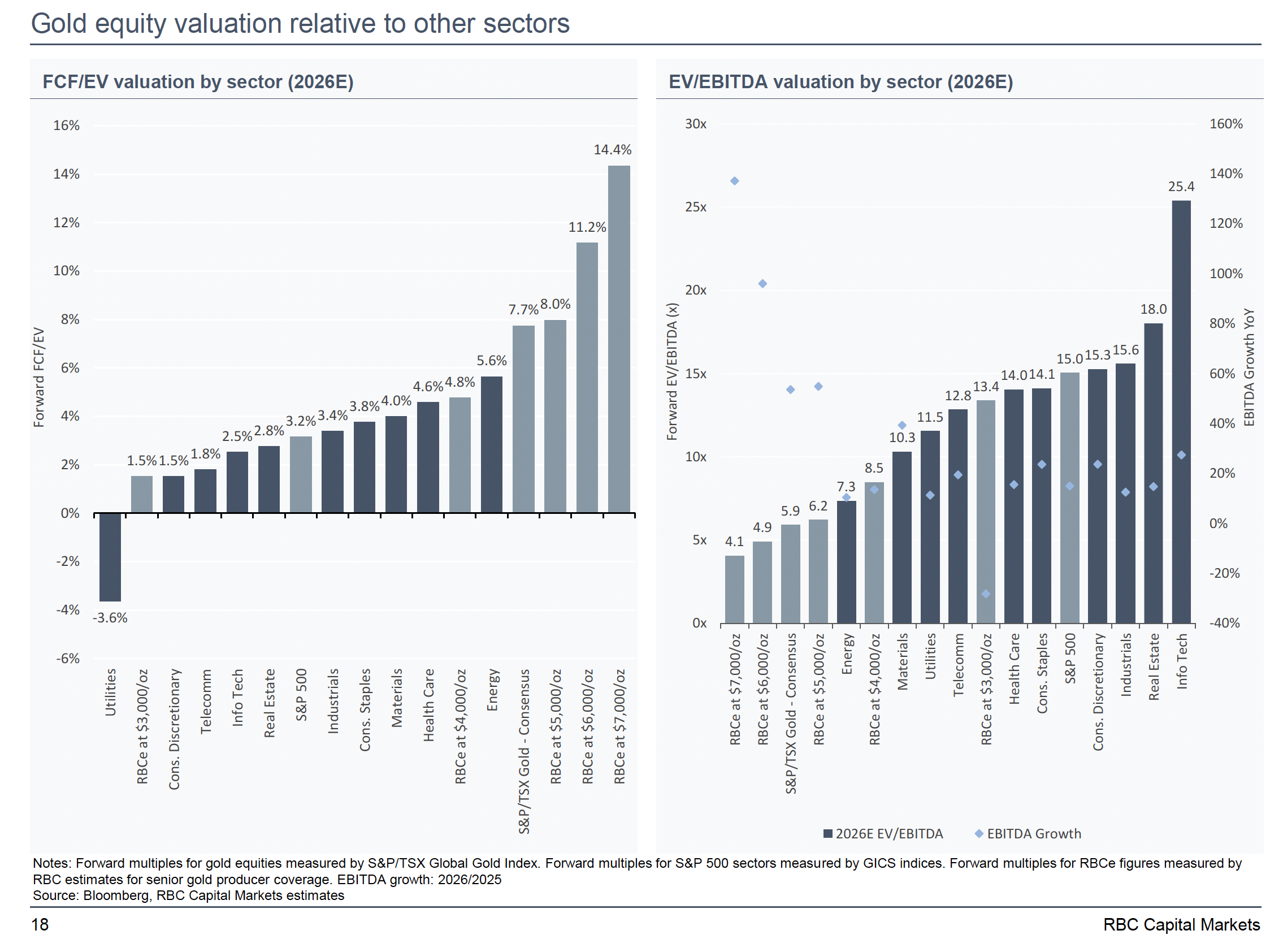

Featured chart

Despite the substantial returns of the past year, gold miners are still trading at relatively attractive valuations compared to the rest of the market, according to RBC Capital Markets, which compares the 2026 forward multiples of the S&P/TSX Global Gold Index against the main S&P 500 sectors under different gold price scenarios. Even assuming prices below current levels ($4,000/oz), gold miners according to this metric would trade as the second cheapest sector of the S&P 500, only behind energy.

Along these lines, we have recently published in the community a detailed analysis of Rio2 Ltd, a gold producer that illustrates well the kind of valuation discounts the sector continues to offer.

Recommendations

In this edition we would like to make a recommendation different from the usual ones. On June 6, Reus will host the 5th anniversary of Charlando de Minas, the podcast led by our partner Amadeu Bonet. It will be one of the few events in the Spanish-speaking world bringing together leading voices from the world of investing in commodities, gold, mining and energy. If you are interested in the topics we cover in this newsletter, this is an excellent opportunity to hear first-hand from those closest to the sector and to connect with other investors and professionals. All information by clicking on the image:

We could not skip recommending an interview we found particularly interesting with a macro analyst we recommend following closely: Warren Pies. In the conversation, Pies explains the two forces that in his reading are moving markets today: on one hand, a genuine explosion around AI, which is feeding a capex cycle and an unprecedented earnings boom; on the other hand, the historic oil crisis derived from the Strait of Hormuz blockade. Despite the energy risk, Pies remains fundamentally bullish on equities, arguing that the AI capex cycle and still-active fiscal stimulus are sufficient for the S&P 500 to look through the energy shock. Essential to understanding why the market is where it is.

With this we conclude the fifth edition of the Truth Below Ground monthly newsletter. As always, we would greatly appreciate your feedback through whichever channel suits you best (links below, or simply reply to this email), not only on this newsletter but also on the reports we have published and on the project as a whole. We look forward to hearing from you!

Until next time.

Disclaimer

The content of this newsletter has been prepared by Truth Below Ground exclusively for informational, educational and research purposes related to the mining sector only. It does not, under any circumstances, constitute financial, legal or professional advice, nor should it be interpreted as a personalized investment recommendation.

All information, data and analysis included are derived solely from public and reliable sources, although Truth Below Ground does not guarantee their accuracy, completeness or validity. This newsletter may contain forward-looking statements subject to risks and uncertainties that could cause actual results to differ materially from the estimates presented herein.

The content does not take into account the objectives, financial situation or specific needs of subscribers. Readers are advised to consult with qualified financial advisors before making any investment decisions.

By subscribing to and using this newsletter, the reader acknowledges and accepts this disclaimer and assumes full responsibility for any decisions made based on the information provided. The total or partial reproduction of this content without prior authorization from Truth Below Ground is strictly prohibited.