Delivering this edition of the newsletter has not been easy, given the constant flow of developments and headline-driven statements that have triggered extraordinary price movements, as well as the complexity and breadth of the events unfolding. Nevertheless, we hope you find it valuable.

The unexpected happened and, after months of rising tensions, war with Iran broke out. With it came the blockage of the critically important Strait of Hormuz and damage to energy infrastructure across the region, with highly significant direct implications and second-order effects that are still difficult to fully assess, but which will undoubtedly have a material impact on the macro environment and across asset classes.

Including, of course, metals and mining equities. The weeks when our sectors of interest were rising almost daily, with strongly positive investor sentiment, now feel distant.

Before diving deeper, we would like to remind you of our latest report on Rio2 Limited, a mining company with gold and copper production operations in Chile and Peru respectively, whose share price has recently declined sharply alongside the sector. A buying opportunity at lower prices? Beyond analysing risks and opportunities across different areas, the report includes a highly insightful valuation sensitivity analysis under different price scenarios.

It is available both to community members —with a special launch offer currently open— and as an individual purchase.

Without further delay, we will attempt to summarise the most relevant developments in the macro and metals environment. While the focus is clearly on the Middle East conflict, we would not like to overlook other underlying trends. Our intention is not to provide an exhaustive analysis of all direct and indirect implications, which would be impossible.

Macro environment

From geopolitical tensions to a systemic shock in the Middle East: the risk of a major energy crisis with multiple ramifications

On February 28th, the United States and Israel launched a military offensive against Iran. In response, Iran initially deployed missiles and drones against Israel and US bases in the region. What initially appeared as a contained escalation has rapidly evolved into a broader geopolitical shock, significantly altering the global macro landscape.

Several weeks later, time is clearly working against a resolution. Before irreversible effects trigger a major economic crisis, the need for an agreement is critical. Trump has therefore stated that additional attacks on Iranian energy infrastructure will be postponed, while also referring to productive talks with Iran — claims denied by Tehran. Can we rely on Trump? Volatility is guaranteed.

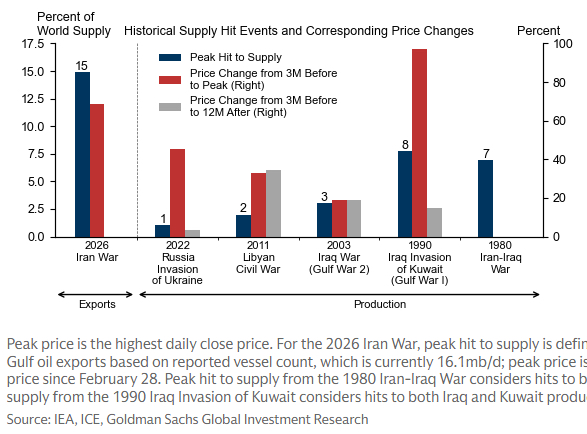

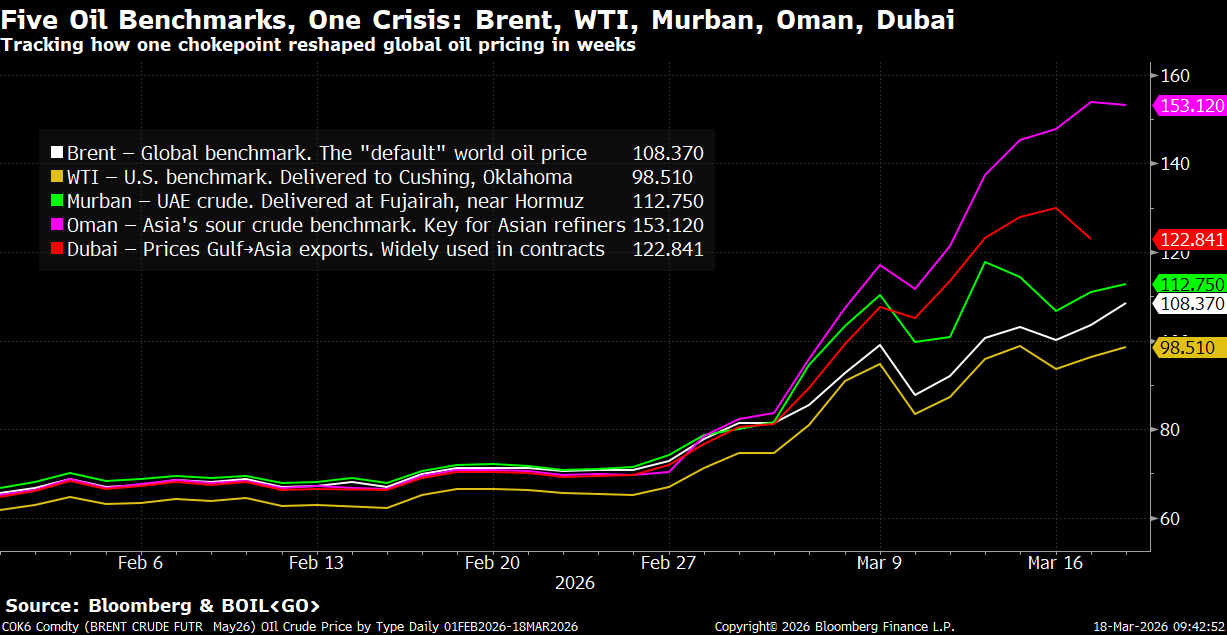

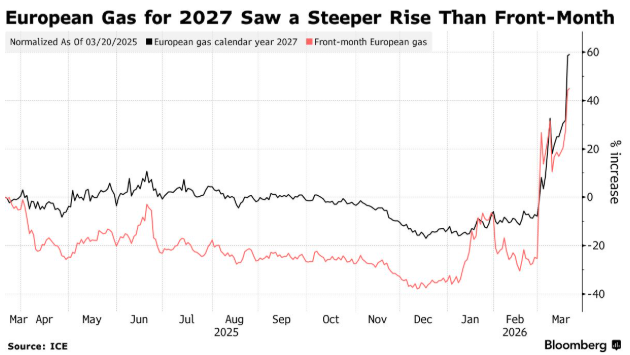

In any case, the most immediate impact of this conflict has been in energy markets, particularly oil, refined products and LNG. The Strait of Hormuz — through which around 20% of global oil and gas flows transit— has seen its traffic reduced to minimal levels since hostilities began. This has been compounded by recent attacks on strategically critical energy infrastructure. Overall, the current situation represents the largest supply disruption in the sector’s history.

The most significant attack affected the world’s largest LNG export facility in Qatar. Its operator, QatarEnergy, has confirmed that approximately 17% of its production capacity has been lost, with repair timelines estimated at three to five years. This point is critical: the market may be underestimating that this is not merely a temporary logistical disruption, but a structural shock to productive capacity.

Even under an optimistic scenario involving a ceasefire or imminent end to the conflict, normalization will not take weeks, but months or years. In this regard, we recommend this reading, which explores how damage to LNG infrastructure — due to its complexity — can evolve into a systemic shock with long-lasting implications for global energy supply.

As expected, fossil fuel prices have surged, particularly refined products such as diesel and jet fuel, with direct implications for economic activity. Oil price reactions have been uneven across regions, with a more pronounced impact in Asia due to its higher dependence on Middle Eastern flows. Analysts suggest that if the conflict is not resolved quickly, prices could continue to rise, as the supply-demand gap that has emerged is unprecedented (more in the Recommendations section). It is difficult to imagine this being resolved with a single tweet from Trump TACOing.

Effects on the dollar and global financial markets

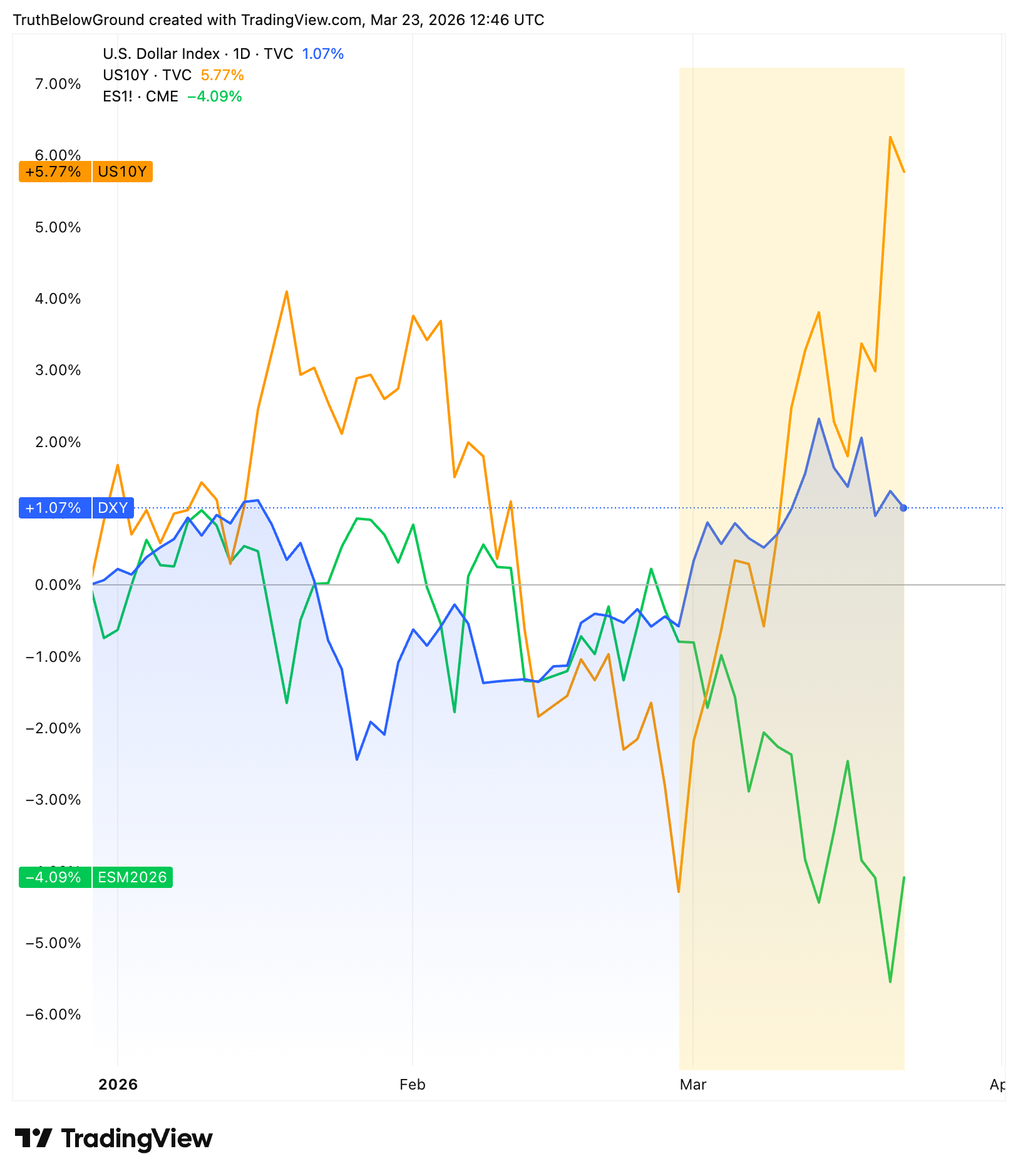

Beyond energy — and it is worth remembering that energy underpins virtually all economic activity — this type of shock has a direct transmission to global financial variables, particularly through the US dollar.

The increase in energy import costs deteriorates trade balances across many countries, particularly in Europe and energy-dependent emerging markets. This generates increased demand for dollars to finance these imports, putting upward pressure on the US currency.

In this context, the dollar tends to act both as a safe haven and as the global funding currency, reinforcing its appreciation during periods of energy stress.

Dollar (blue), US equities (green) and US 10-year yield (orange) in 2026

Note: the orange line represents bond yields (inverse of bond prices).

However, there is a second, less visible derivative effect highlighted by some analysts, although evidence remains limited so far: energy-importing countries — particularly in Asia (as well as Gulf countries whose export revenues have declined) — not only require more dollars, but in many cases must generate liquidity to absorb the increased cost. How? By liquidating assets, introducing downward pressure on bond markets, equities, and —as we will discuss later— gold.

In other words, the energy shock tightens financial conditions, acting as a drain on global liquidity.

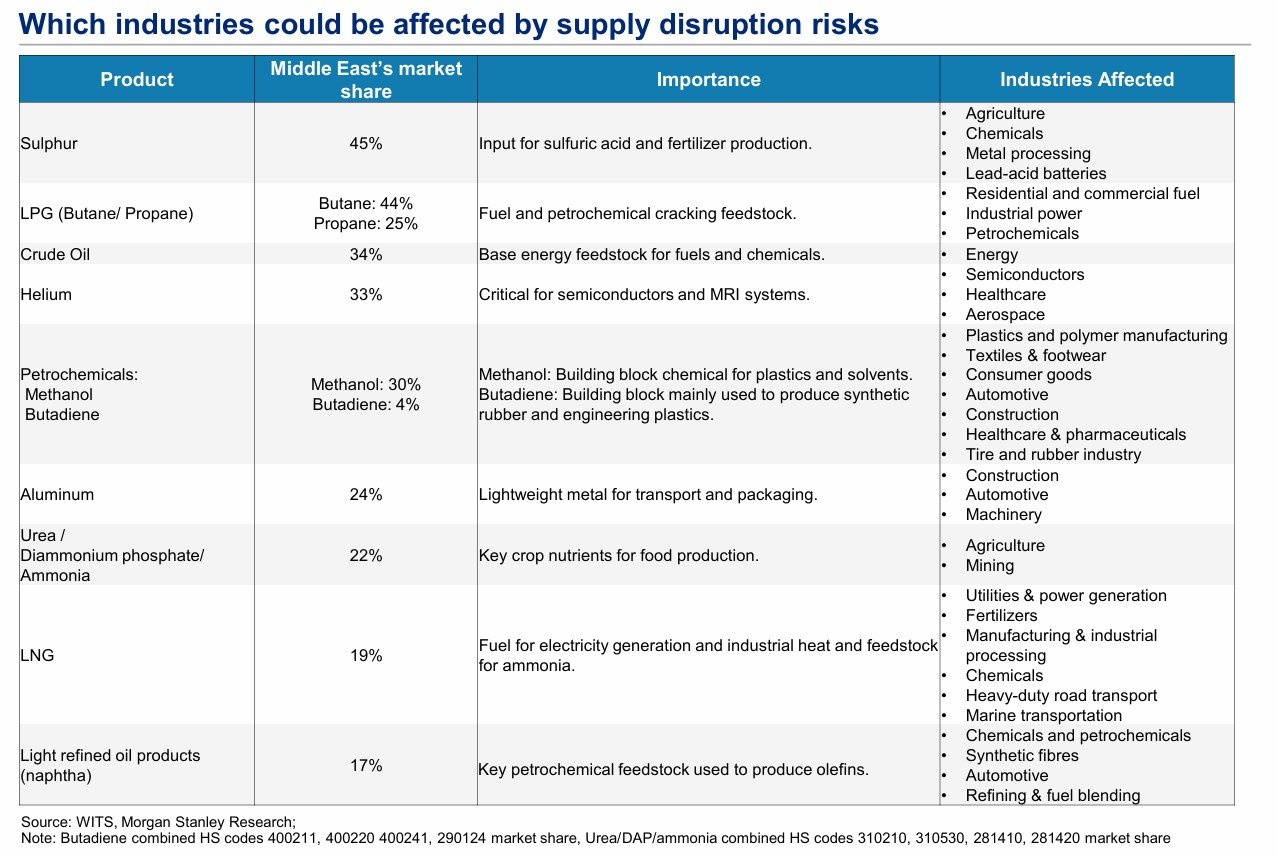

Returning to the real economy, another key issue is the impact on critical value chains, particularly fertilizers (among others, such as helium), and what this implies for global food security. The Strait of Hormuz is a key transit route for essential compounds such as urea and sulphur. The consequences for emerging markets could be severe. Central banks will need to closely monitor these second-order inflationary effects, which tend to materialise with a lag —crop yields adjust months later, not immediately.

This shock serves as a reminder of the deep dependence on fossil fuels across multiple areas of the economy:

At the same time, we should briefly mention other topics. Prior to February 28th, the dominant narrative was centred on the impact of artificial intelligence on the economy and financial markets. Announcements from major AI players such as Anthropic triggered sharp declines across sectors including software, insurance, legal services and finance. In contrast, capital-intensive sectors with tangible assets, such as natural resources, proved more resilient.

From a macro perspective, AI was seen as potentially deflationary, through labour displacement and productivity gains, supporting a bearish narrative for US Treasury yields (the 10-year briefly fell below 4%). The conflict in Iran abruptly reversed this trend, reintroducing inflation concerns and pushing yields higher.

Another factor now pushed into the background is the controversy surrounding Trump’s tariffs, following the Supreme Court’s partial invalidation of his tariff programme. This has implications for US fiscal dynamics, and therefore for the dollar and gold.

The Fed and stagflation risk

In this context, the Federal Reserve, in its March 18 meeting, acknowledged extreme uncertainty and maintained its “wait-and-see” stance. Powell highlighted upside risks to inflation and downside risks to employment — a highly challenging combination for policymakers. The market still remembers the impact of rate hikes in 2022.

Stagflation risk has therefore increased significantly. However, equity markets have not yet reacted meaningfully, suggesting that investors are still pricing in a rapid and painless resolution. But is that realistic?

Are we facing a temporary shock, or the early stages of a deeper energy crisis comparable (though not identical) to the 1970s? Some analysts even suggest this chain of events could be as disruptive as COVID — but in the opposite direction for oil.

Historical analogies always have limitations. But in this case, the similarities are strong enough to warrant caution — despite recent statements from Trump suggesting a desire to de-escalate, likely due to the extremely high and unsustainable costs involved.

As a final reflection: what does this episode tell us about the true extent of US geopolitical power, when an apparently weakened actor such as Iran is capable of stressing a system as critical as global energy supply?

Metals markets

Contagion effect, where are the safe havens?, towards greater emphasis on security of supply of strategic natural resources

Gold and silver

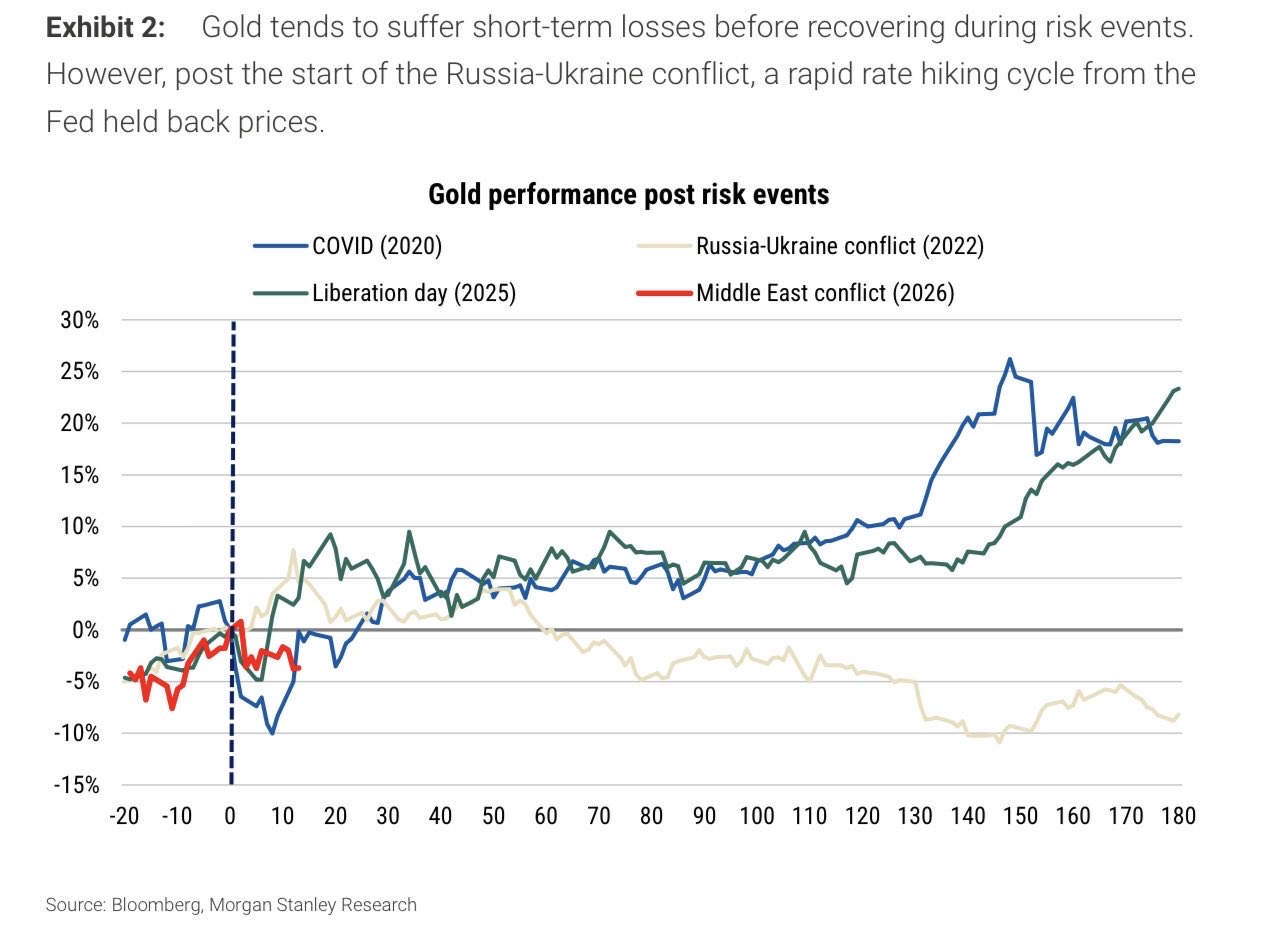

In the macro scenario we have outlined, the movement in gold has been particularly striking. While many expected it to fulfil its traditional role as a safe-haven and diversifying asset during periods of turbulence (as initially occurred), we have instead seen a sharp decline that has led some to question whether we may be witnessing the end of the bull market in precious metals.

Gold (orange) and silver (grey), % performance in 2026

Existen varias hipótesis, no excluyentes entre sí, que circulan entre los analistas, que merece la pena exponer brevemente:

Gold as a “procyclical” asset driven by reserve flows

This is perhaps the most structural and novel hypothesis in the current debate, notably put forward by Michael McNair. The argument is that, following the freezing of Russian reserves in 2022 and the “weaponisation” of the dollar, countries with trade surpluses — particularly GCC nations and China — have shifted away from US Treasuries and rotated massively into gold as a neutral reserve asset.

This would have transformed gold into a more procyclical asset, dependent on reserve flows from these countries rather than traditional drivers such as real interest rates or volatility. The decline in oil production in the region and the disruption in the Strait of Hormuz — as discussed earlier — has reduced GCC revenues, forcing them to generate liquidity and potentially slow or reverse gold purchases. Other emerging markets could face similar dynamics.

The result: gold declines precisely when, under its traditional safe-haven role, it would be expected to rise. The structural thesis may remain intact, but the metal appears to have become more volatile and more correlated with the global cycle.

Forced selling amid a strong dollar and shifting monetary expectations

Another complementary interpretation is that gold’s decline may be driven by forced selling from both retail and institutional investors, either to cover losses in other assets or to reduce overall portfolio risk (de-grossing), with correlations temporarily converging towards one — as seen in March 2020 or in recent episodes of market stress.

At the same time, a stronger dollar and expectations of tighter monetary policy, driven by renewed inflationary pressures, represent clear headwinds for gold. Given its high liquidity and strong recent performance, gold may be sold as collateral damage in broader portfolio adjustments.

Profit-taking after the rally and tactical rotation into energy

Gold experienced a sharp rally throughout 2025 and into early this year. Investors sitting on significant unrealised gains may have decided to rotate into oil, fertilizers and other assets more directly exposed to the current shock.

Corrections of this nature are typical within broader bull markets. As the saying goes, bull markets do not rise in a straight line — something gold seemed to challenge in previous years, but which recent developments have once again confirmed.

What can we expect in the medium term?

Although in the short term — particularly in a severe risk-off scenario or if markets begin to price in a more hawkish monetary response — the correction could deepen, we believe that gold’s structural fundamentals remain intact. A stagflationary environment has historically been supportive for the metal.

However, the perception that gold may have become more procyclical raises questions about the extent to which its traditional correlations and safe-haven role remain fully reliable under this type of shock. That said, it is still too early to draw firm conclusions in an environment of elevated volatility and complexity, where multiple forces are interacting simultaneously.

Regarding silver, given its dual role as both a monetary and industrial metal, its price will also be influenced by expectations of slower economic growth. However, should investment in solar energy accelerate as part of efforts to diversify away from fossil fuels, silver demand could benefit from this trend.

Are you a company or an institutional investor in need of an expert, multidisciplinary, and independent evaluation of mining projects? We may be able to help.

Copper

Copper has corrected from its January 29th highs, in a context of relatively weak physical demand and elevated macro uncertainty. Inventories in key markets — as we have discussed in previous newsletters — have risen significantly and are now at multi-decade highs, partly reflecting global dislocations driven by trade frictions.

Copper price performance in 2026

The Iran conflict introduces additional variables that deserve attention. On the demand side, a deterioration in global economic growth — with early signs already visible, particularly in parts of Asia — could translate into weaker industrial copper consumption.

On the supply side, the most immediate channel is sulphuric acid. This input is critical for oxide copper leaching, the dominant processing method in the DRC Copperbelt, the world’s second-largest copper-producing region. Sulphuric acid is produced locally from imported sulphur, and according to Robert Friedland, CEO of Ivanhoe Mines, more than 90% of sulphur imports into Africa originate from the Middle East and transit through the Strait of Hormuz.

With the Strait effectively closed, operators are already facing difficulties securing supply. If disruptions persist, oxide copper operations in the region may be forced to reduce or halt production due to lack of acid. At the same time, rising energy costs are adding further pressure — not only on mining operations, but particularly on smelters.

Structural medium- and long-term fundamentals remain constructive. The likely acceleration of electrification — through investment in transmission, distribution and renewables — would act as a tailwind. However, in the short term, the balance of forces remains uncertain and warrants caution.

Critical minerals (lithium, uranium, rare earths… tungsten!)

There would be much to discuss regarding each of these minerals individually, but given the length already reached, we will limit ourselves to a few general remarks.

Once the current shock subsides, one of its most lasting effects may be a renewed focus on supply security and the reconfiguration of global value chains for critical minerals — with greater regionalisation, stronger alliances between aligned countries, and reduced dependence on dominant single suppliers.

For example, in rare earths, US aerospace and semiconductor suppliers have warned of growing shortages of yttrium and scandium, almost exclusively produced in China. Given their importance in military applications, rare earths will remain a strategic priority for the US government in its dealings with Xi Jinping.

A particularly notable case is tungsten, whose price (ammonium paratungstate) has surged from below $400 per tonne a year ago to over $2,200. Two main factors explain this move: China has significantly restricted exports, and each missile used in the Iran conflict consumes tungsten irreversibly — unlike industrial uses, it cannot be recycled — draining inventories in an already tight market.

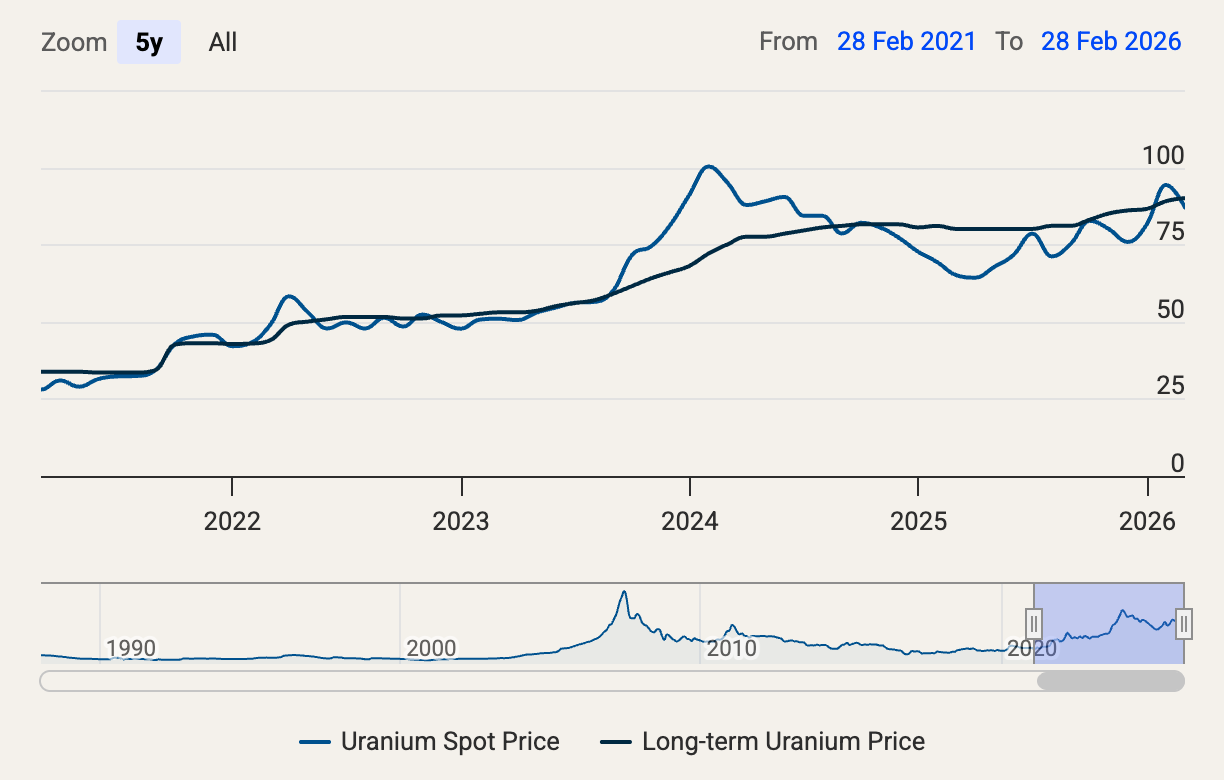

In the case of uranium, nuclear energy could receive renewed support from governments, as seen after the war in Ukraine, recognising its role in providing stability and security to power systems. However, vulnerabilities remain in the nuclear fuel cycle, where Western utilities lag behind countries such as China or India in securing long-term supply.

Source: Cameco.

Truth Below Ground is a mining investment community powered by a multidisciplinary team of industry professionals. Risk and opportunity analysis from a truly technical perspective.

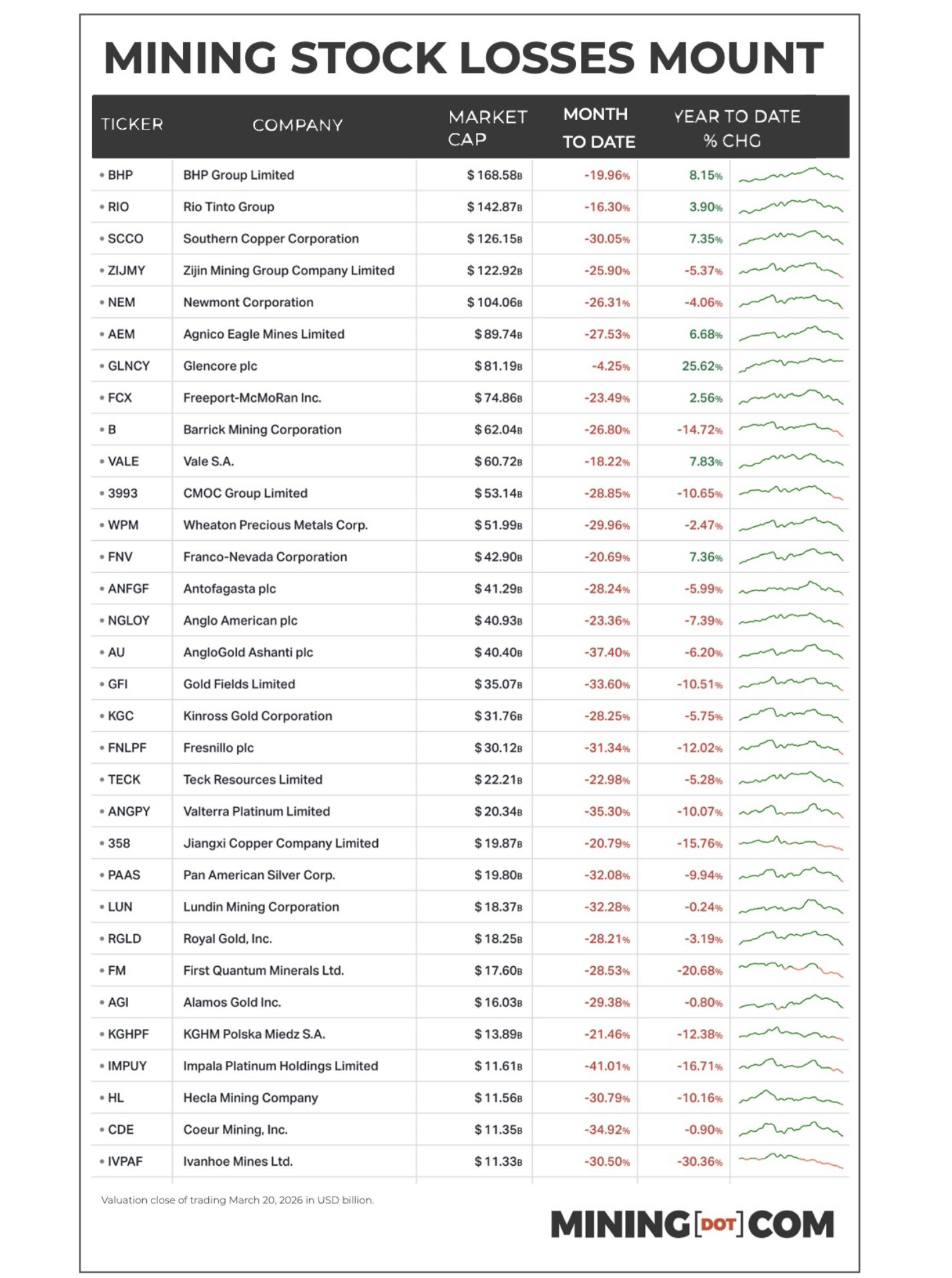

Mining sector

In this environment of declining metal prices and rising cost inflation (more on this in the featured chart), mining equities have undergone a sharp correction, as reflected in the table below (as of Friday the 20th, showing the largest companies in the sector):

Via Lobo Tiggre

In the following chart, we show performance by segment across different timeframes, including Monday’s rebound following Trump’s statement regarding potential negotiations:

Source: Investing.com as of March 23.

Interestingly, most sectors remain in positive territory for 2026 despite the recent correction, reflecting the strength of the previous rally — a factor that may also have intensified the drawdown.

Additional resources

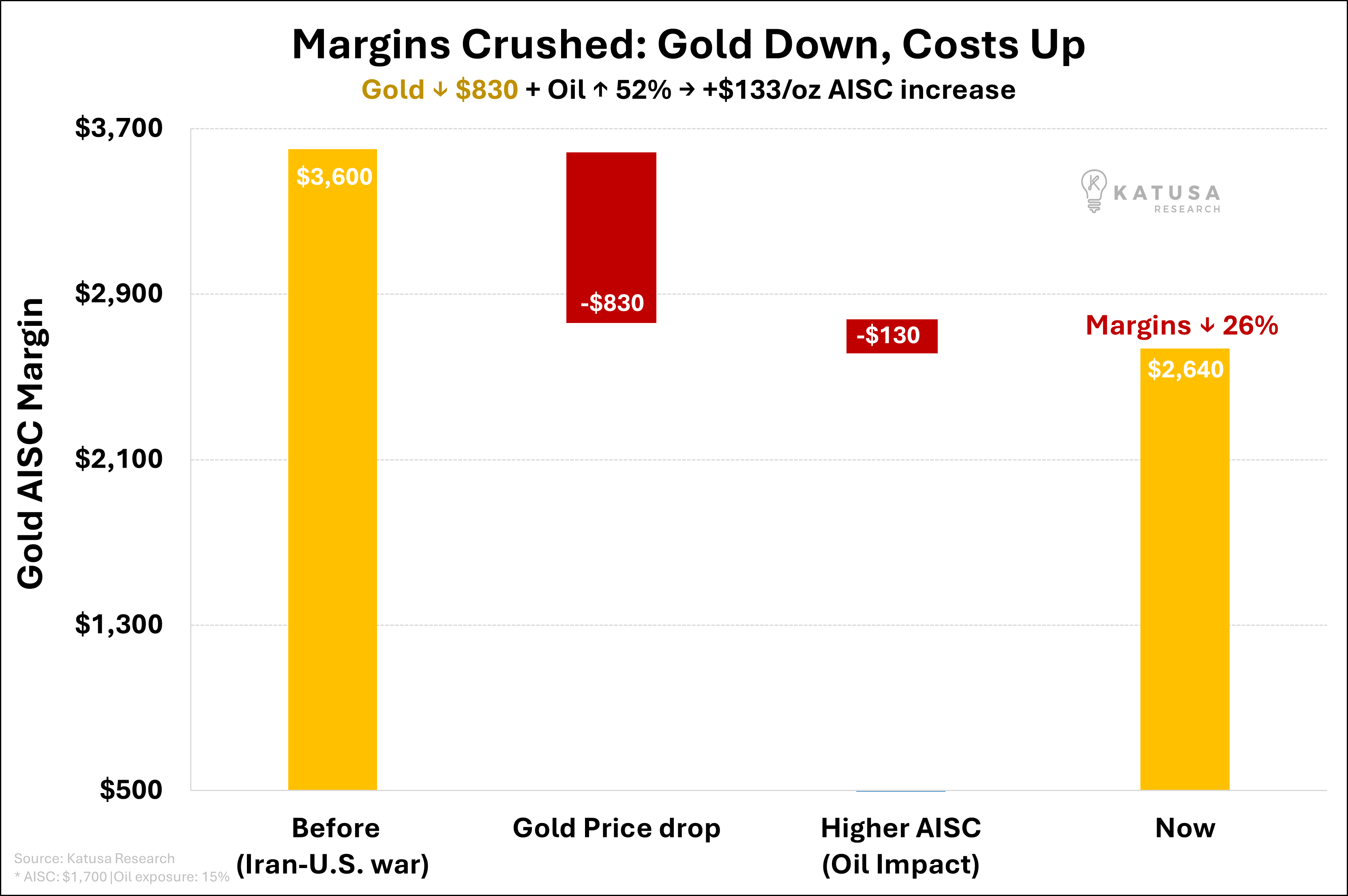

Chart of the month

Specifically for gold miners, the decline in gold prices combined with rising energy costs has eroded a portion of the exceptional margins these companies have been enjoying — although this will not yet be visible in Q1 financial results:

However, the impact of rising oil prices could be greater than shown in the chart. First, because refined products such as diesel have risen more than crude. And second, because higher energy costs may feed into broader inflation across inputs such as explosives, chemicals, food, and labour transport, as highlighted by @respeculator.

The impact will vary across mines depending on their fuel sourcing strategies, supply chains, and other operational factors.

Recommendations

As expected, we bring two key recommendations to better understand the current situation.

The first focuses on the oil market, featuring sector analyst Rory Johnston, who outlines potential scenarios depending on the actions of key geopolitical players — both for oil prices and the global economy. Spoiler: he believes maintaining the status quo would be so catastrophic that his base case remains a rapid agreement (the so-called “TACO” scenario). Otherwise, the risk of $300 oil — and with it a global depression — remains on the table.

The second provides a broader macro perspective with Luke Gromen, highlighting the importance of the bond market as a key indicator of systemic stress. Among other points, he argues that while Iran cannot defeat the US militarily, it could exert pressure through the bond market, given the system’s excessive debt.

We will continue to closely monitor developments in order to provide you with high-quality analysis. In the meantime, remain calm and fasten your seatbelts — volatility is here to stay, along with the opportunities it creates.

With this, we conclude the fourth edition of the Truth Below Ground monthly newsletter. We would greatly appreciate your feedback!

Until next time,

Disclaimer

The content of this newsletter has been prepared by Truth Below Ground exclusively for informational, educational, and research purposes related to the mining sector only.

It does not, under any circumstances, constitute financial, legal, or professional advice, nor should it be interpreted as a personalized investment recommendation.

All information, data, and analysis included are derived solely from public and reliable sources, although Truth Below Ground does not guarantee their accuracy, completeness, or validity.

This newsletter may contain forward-looking statements subject to risks and uncertainties that could cause actual results to differ materially from the estimates presented herein.

The content does not take into account the objectives, financial situation, or specific needs of subscribers. Readers are advised to consult with qualified financial advisors before making any investment decisions.

By subscribing to and using this newsletter, the reader acknowledges and accepts this disclaimer and assumes full responsibility for any decisions made based on the information provided.

The total or partial reproduction of this content without prior authorization from Truth Below Ground is strictly prohibited.